May’s Top Take – Earnings Make the World Go Round

If May proved anything it’s that earnings seasons can quickly change the market narrative. Even though the economy rose merely 1.6% in the first quarter on lackluster consumer spending growth, it was a banner quarter for US companies amid rapid acceleration in AI investment with profits rising nearly 30% in a rare mid-cycle boom. As a result of the earnings surge and signals of continued investment from large tech companies, strong growth is now assumed as the base case for 2026 across markets.

Herein lies the challenge for the months ahead. Profits may continue to surge at a breakneck pace given the seemingly endless quest for AI among tech titans, but there is no such thing as a free lunch – growth has a cost when it is so concentrated, and the combination of tech-specific growth with geopolitically disrupted supply chains could result in inflation becoming disruptive as the second half of the year approaches. Inflation is already rearing its ugly head again – a development that equities are currently assuming is transitory, but data suggests otherwise. As the recent bout of higher prices is in part driven by the AI-investment that has been fueling earnings gains, a challenging feedback loop may be at play whereby accelerated tech sector investment continues to drive both profits and prices higher, but consumers struggle to keep up. Treasuries appear more accepting of this fact with the yield curve failing to meaningfully steepen even as the long end remains stubbornly high.

As earnings season winds down and economic data moves center stage for markets, policymaking from the Federal Reserve may become the focus. Under new leadership hungry to enact change, the group will have its work cut out for it as they attempt to balance shorter term supply pressures from the conflict in Iran with longer-term demand-driven inflation, as well as exuberance in financial markets and corporate profits with stagnation in labor markets and household spending.

May Was a Strong Month for Stocks.

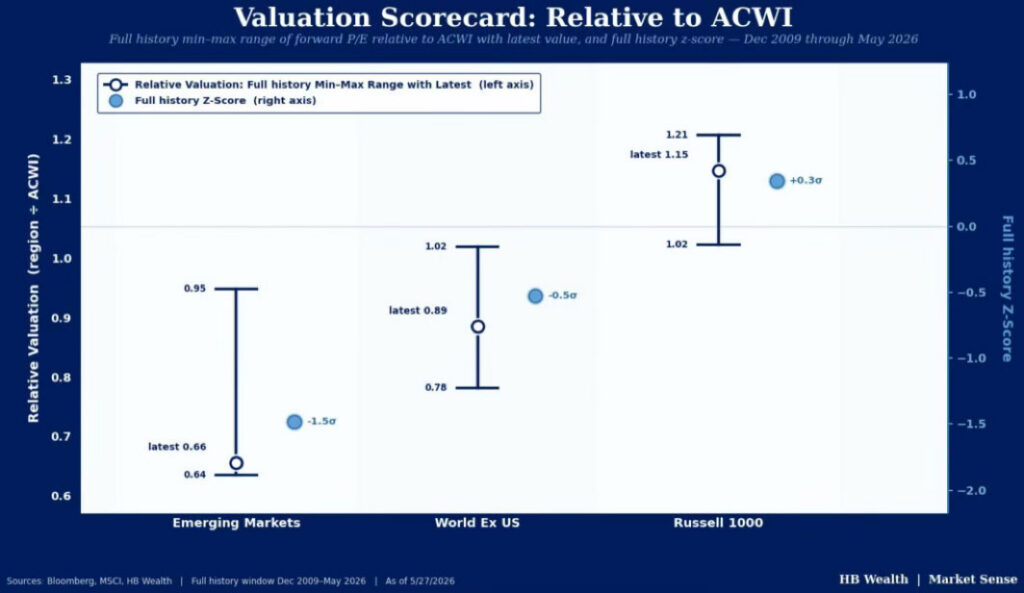

All major US indices climbed in May, powered by a strong earnings season and prospects for a resolution to the conflict in Iran. Large caps led the charge, followed by the Russell 2000 with growth outperforming across capitalizations. Performance was split by sector – in the Russell 3000, tech, telecom, health care, materials and discretionary led while energy, utilities, financials, staples, real estate and industrials slipped. Emerging markets continued their torrid performance, rising 9.5% thanks to surging tech stocks. We outline how despite rising tech concentrations in Emerging Markets, the group still maintains a relative valuation discount and can provide a diversification benefit here.

Earnings Were the Main Catalyst Last Month.

Both S&P 500 and Russell 2000 earnings lapped consensus forecasts, aiding stocks’ rise for the month. With just 3.5% of index market cap left to report (mostly Broadcom which is set to release on June 3rd), the S&P 500 is on pace for a 29.4% year-over-year earnings gain versus the preseason forecast for 12.4%, and 83.5% of companies cleared their respective hurdles. Tech posted the strongest earnings growth, followed by communications and materials. The Mag-7 saw earnings rise 58.8% (for more on the Mag-7 see our Market Sense here), but even excluding this group, index earnings rose 17.3% — the best mark since 4Q21. With about 5% of its market cap left to report, the Russell 2000 is on pace for a 7.4% revenue gain versus the preseason consensus for 4.8% and 58% of companies beating expectations. Materials, real estate, tech and financials posted the strongest top-line growth in the small cap gauge in 1Q. The analyst consensus sees strong earnings growth continuing – their expectations for growth in coming quarters have marched higher across capitalizations.

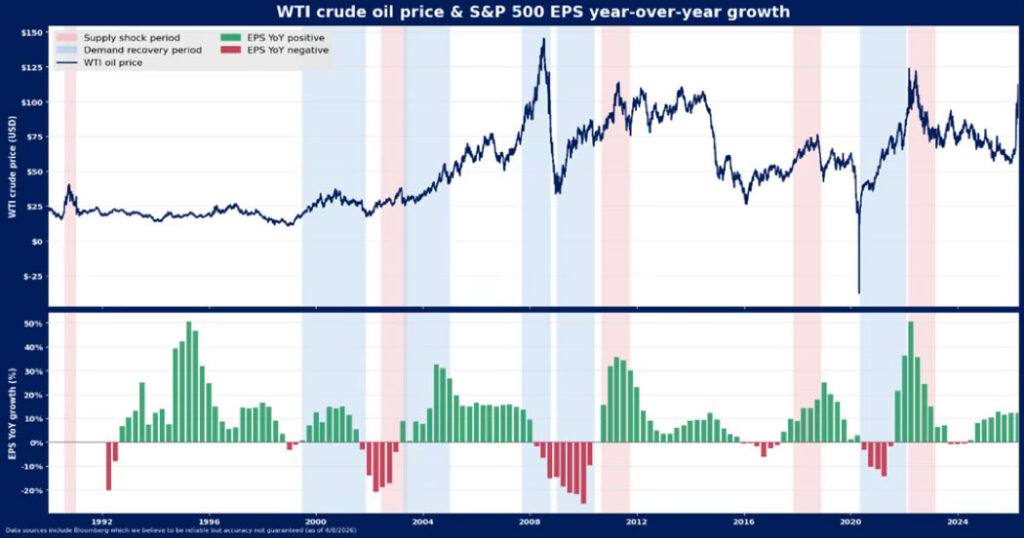

Oil Remains Volatile and Elevated, Watch For Bumps in 2Q Earnings.

With the second quarter now 2/3rds in the books, the higher earnings prices that have persisted for a majority of the reporting period could cause some bumpy results once companies begin to release 2Q earnings in early July. West Texas Intermediate (WTI) crude closed May just a tad below $90/bbl and was whipsawed throughout the month by headlines around the conflict in Iran. Brent crude remains substantially higher than WTI given higher foreign reliance on oil from the Gulf region than the US. Nonetheless, WTI is roughly 70% higher than at the start of the year and in the 88th percentile of observations back to 1995. Oil hits earnings with a lag, and may cause some earnings disruptions in coming quarters, as we laid out here.

Bonds End the Month Little Changed.

Yields briefly touched 2026 highs in May before pulling back. The 10-year yield rose roughly 73bps at its peak before retracing roughly 23bps of that on the back of easing energy prices, with a net move of roughly 6.5bps higher on the month. The broadly quoted Agg index returned 0.31%, with income as the primary driver. A modest rates headwind was largely offset by mild spread tightening. Seasonal tailwinds led the municipal market to lead taxables by 6bps for the month, before accounting for tax benefits.

Inflation Remains Key to Equity Outlook.

Of May’s cycle of economic releases, the various inflation readings were the most important to the outlook. Both CPI and PPI Final Demand came in hotter than consensus forecasts and while core PCE – the Fed’s preferred metric – met forecasts, at 3.3% it’s still well above target. FOMC meeting minutes showed a growing list of governors that would prefer the next move from the central bank to be a hike while market expectations have quickly shifted to suggest a full hike is possible by January 2027. It appears we may be entering a new regime where inflation is policymakers and investors’ top concern, rather than growth, as outlined here.

IPO Surge is in Full Swing, Even Before SpaceX’s June Issue.

SpaceX is expected to IPO around June 11th in what will be the largest offering ever that, if combined with possible OpenAI and Anthropic IPOs later this year will put 2026 in the history books (for more on mega-cap IPOs, see our deep dive here). In May, however, we got the much-anticipated IPO of Cerebras. Following a very successful offering, the chipmaker is up 20.5% from its IPO price, possibly offering a look at what’s to come.

Keep an Eye On Stocks’ Disappearing Risk Premium.

The large cap equity risk premium (ERP) – the difference between the earnings yield on stocks and the 10-year TIPS yield – is at levels last observed around the 1999-2000 tech bubble. Much of the recent drop can be attributed to higher real yields. While stocks have enjoyed strong returns in period where the ERP was chronically low, a slip into the lowest quartile of risk premia likely signals slowing expected returns for equities as an asset class. For more on the equity risk premium, see our Deep Dive here.

Chart of the Month

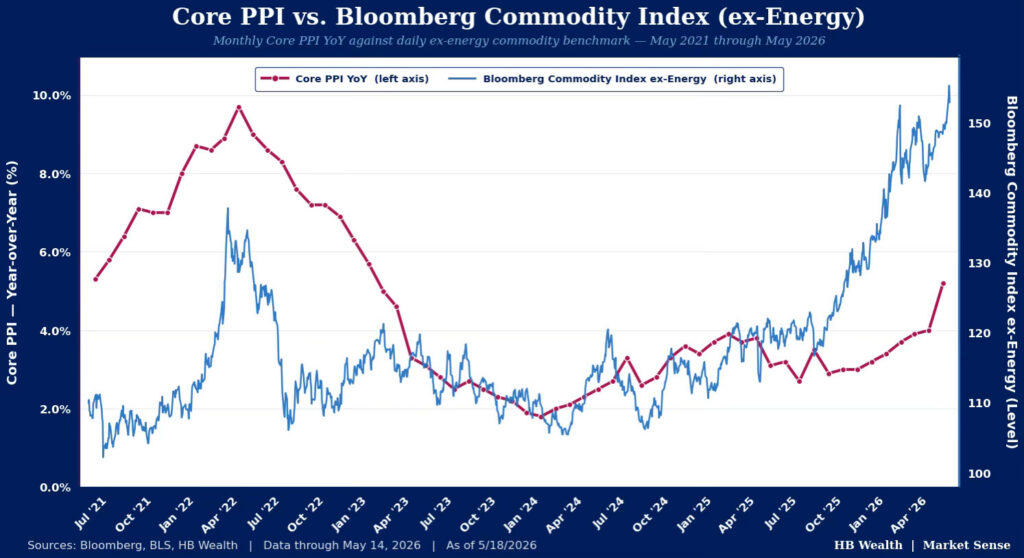

The AI spending boom has one potentially underappreciated risk, and that’s its near-term inflationary impact. Consumer and producer prices rose much faster than expected in April and the price gains aren’t easily dismissed as all related to war-time costs. Indeed, the continued elevation of spending by tech companies appears to be sparking a wave of inflation in ex-energy goods prices. Hyperscalers’ plans to spend more than $700 billion in 2026 and another $1 trillion in 2027 building AI infrastructure implies inflation risks may remain, even if supply constraints in the Middle East are resolved.

Disclosure: HB Wealth is an SECregistered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.