Abstract:

2026 could be the best year for IPOs on record based on already completed deals and the expected size of SpaceX, OpenAI and Anthropic offerings.

Due to its low float shares outstanding, SpaceX’s effect on the S&P 500 could be limited to start. If OpenAI and Anthropic follow a similar path, their additions will mean more for respective sector concentrations than for the index at large.

The 10 biggest US IPOs in history may provide some insight into what performance could look like. Index additions appear to matter more than the IPO itself for both index and associated sector performance.

Bevys of IPOs in the past have coincided with major market tops in 1999-2000, 2007 and 2021. This surge is just one signpost that overall risk tolerance might be getting overheated. If performance following issue is stronger than historical norms, we suggest crossing IPO signals with other measures of market sentiment.

The Fed may have a hand in determining how long and how far the IPO cycle extends. Since the pandemic, periods where rates were falling have boosted IPO prospects while hikes have choked off issuance.

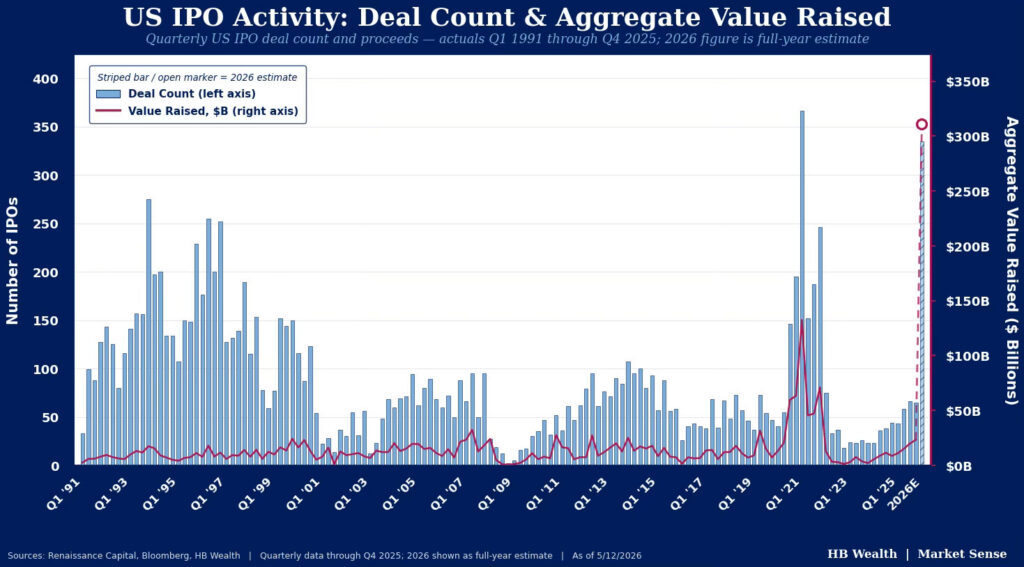

2026 is set to see a bevy of record-breaking IPOs between SpaceX’s anticipated offering in June to OpenAI and Anthropic later this year. Surges in IPO deal values have typically occurred near major tops as private investors and C-suites look to hit the market at the best valuation possible and 2026 just might be the best year on record for offerings going back to 1990. However, while their valuations are sky high, the impact of these new issues may be muted by the small amount of shares (the free float) that will be available to the public, and their timing for index inclusion, which is likely to be uniquely immediate. SpaceX is already setting a precedent, seeking $75 billion of funding on a $1.75-$2 trillion valuation – roughly a 3.75-4.2% float. Typically, S&P requires 10% of shares floated to be considered for inclusion, but index providers are already rushing to change their rules to expedite inclusion for these stocks. Historical performance following the US’ 10 largest IPOs is notably mixed, but their eventual inclusion in the index and sector-specific ETFs appears to lend a bid. Given the S&P 500 is weighted by float shares, 2026’s IPOs are unlikely to change extreme index concentration in the magnificent-7 – at least until additional shares come to market via lockup expirations.

Possible Record-breaking Year For IPOs Caution on Elevated Risk Tolerance

2026 could easily surpass 2021 as the strongest year for US IPOs on record on the merits of SpaceX, Anthropic and OpenAI alone. SpaceX is poised to be the largest US company to ever IPO when it finally goes public in June or July of this year, but it’s not alone. OpenAI and Anthropic are also expected to IPO later this year with their expected market cap likely putting them at the second and third largest issues ever. Based on IPOs that already occurred plus SpaceX’s $75 billion offering and an expectation that OpenAI and Anthropic will float the minimum 10% typically required for index inclusion ($100 billion each), 2026 could see a total deal value of $310 billion – eclipsing 2021’s $296 billion. But it’s not all blue skies for markets as recent surges in issuance have often preceded bear markets for stocks. In the lead up to the bursting of the dot-com bubble in early 2000, IPO deal values crossed $20 billion for the first time in 4Q99 and remained elevated through 2Q00. The S&P 500 ultimately peaked in 1Q00 but remained near all time highs through early September before sinking 49.2% peak-to-trough. Likewise, another break above $20 billion in issuance from 4Q06-2Q07 occurred just before the October 2007 all time high that was the last before the Great Financial Crisis.

Lastly, surging IPO values from 2Q20-4Q21 following extremely easy money policies that culminated in a massive, $132.5 billion quarter in 1Q21, directly preceded the 2022-23 bear market. While there have been other spikes in IPO activity in 2010, 2012 and 2013 that didn’t result in a downturn, increased activity should provide investors with plenty of good reason to question if the market is getting overheated.

Perhaps IPO performance immediately after going public coupled with deal values provides a true read on excessive risk taking behaviors in the market. In 1999, US IPOs gained an average 88% in the month following issuance and averaged 57% in 2000 despite the start of the dot-com bubble crash – the two best years on record back to 1998. In fact, this thinking has a clear economic linkage – while often some of the fastest growing companies in public indices, IPOs also have significantly less public financial history than established peers, making them quite a bit riskier. However, while 2021 was a clear mini-bubble, especially among small caps, that year only saw IPOs average about a 14% (excluding SPACs) — stressing the need to rely on other sentiment measures to determine major near-term tops in the market.

Where will SpaceX, OpenAI and Anthropic Rank in the S&P 500?

With various providers thinking of changing index inclusion rules to more quickly accommodate the influx of mega-cap IPOs, ETFs and other products that benchmark to these gauges will have to quickly adjust, raising some concerns about market liquidity and possible volatility.

However, the impact, at least in the S&P 500, could be curtailed by the proposed number of shares being offered to the public – also known as the float. Based on SpaceX’s supposed valuation of $1.75-2 trillion and the company’s desire to raise $75 billion with the IPO, SpaceX would make just 3.75-4.2% of shares available to the market. Nasdaq typically requires a 10% minimum float but that threshold has been dropped. Even if SpaceX’s float rose to that threshold following any lock up period, the company’s weight would fall between Analog Devices and McDonald’s in the index’s pecking order. SpaceX would be the 53rd largest stock weight in the index, assuming a $2 trillion valuation. Likewise, assuming a $1 trillion valuation for OpenAI and Anthropic would put those companies around 113th if they were to float 10%.

High Profile IPOs Historically Coincided With Tough Market Performance But Timing for Index Inclusion May Offer Key Support

Concerns that these very large IPOs might suck up a lot of liquidity and lead to volatile markets appears to have some backing. The top 10 largest US company IPOs – Visa (2008), Facebook (2012), GM (2010), Rivian (2021), AT&T (2000), Kraft (2001), Uber (2019), Medline (2025), UPS (1999) and Lineage (2024) – were associated with a median 2.5% gain in the Russell 3000 over the one month after going public. However, on a next-12-month basis, the broad US market was up just 1.5% due to several high-profile IPOs right around market peaks before or during recession.

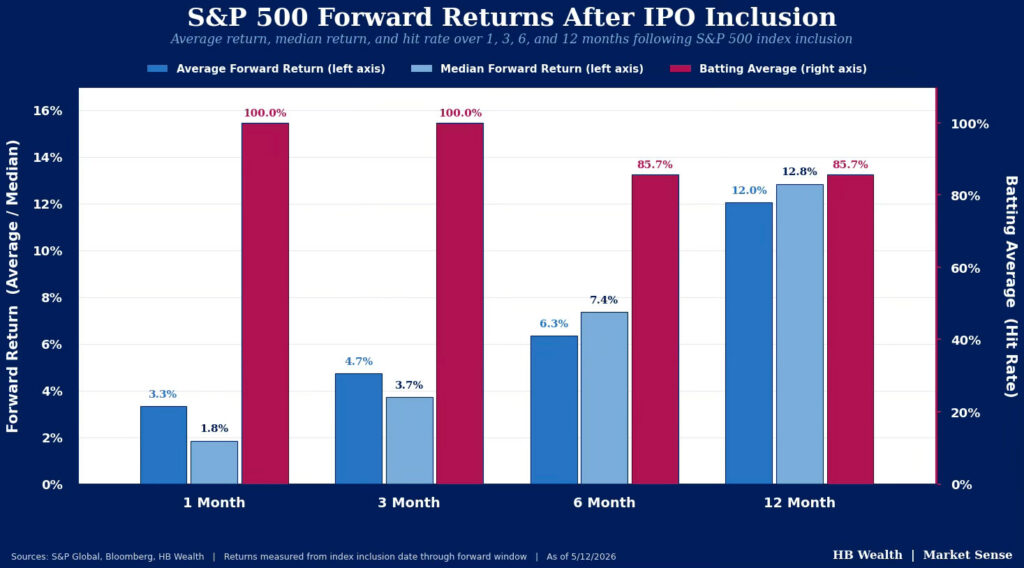

While 2026’s bulky IPO market may signal ebullient confidence, the timing for index entry for these new large issues may somewhat offset the risk to markets, at least in the short run. Index inclusion of large companies historically has resulted in positive returns, because inclusion means forced passive ETF buying. Across those 10 IPOs, seven eventually made their way into the S&P 500 and on median, the index was up 1.8% and 3.7% in the one and three months following. The market also rose in all instances – even on a 12-month forward basis, the gauge gained a median 12.8% and was up following each’s inclusion (except for Kraft Foods in 2007). In 2020, after the stock was publicly traded for a decade, Tesla was added to the index as one of its largest ever inclusions – perhaps a solid corollary to SpaceX’s addition. Like the other sizable index additions, the S&P 500 rose 1.6% and 5.6% in the following one and three months after its inclusion with the index finishing the subsequent year up 24.6%. This evidence suggests the unique timing of index inclusions for 2026’s issues may be a mitigating factor, as demand via passive vehicles will rise to meet the new supply almost immediately.

Index Inclusion Date Matters More For Sector Performance

Large IPOs likewise had little effect on the sectors they were assigned to – at least until they were added to the S&P 500. Across the 10 largest US IPOs, the sector being added to was up just a median 0.9% and 0.8% in the one and three months after going public. Like the overall reading, performance in the year after issuance was muted (down 0.3% on median) thanks to several recessions and market downturns occurring near these major listings. However, once added to the index, performance recovered. The seven stocks that eventually made it into the S&P 500 caused their sector to rise a median 2.5% and 5.4% in the one and three months after inclusion and those groups experienced a 14.5% gain in the year after. Likewise, following Tesla’s addition to the S&P 500 consumer discretionary sector, the sector gained 3% in the following month and 19.9% over the next year.

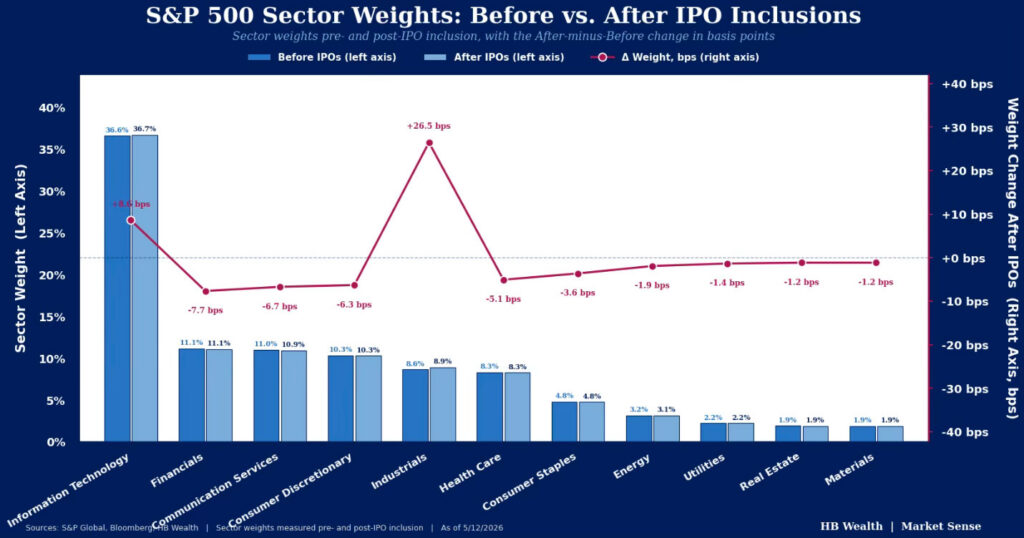

Given the low float that SpaceX is set to IPO with and the precedent it could set for other mega-IPOs like Anthropic and OpenAI, this year’s issuance looks unlikely to relieve much concentration risk in the S&P 500. However, SpaceX’s inclusion could bring in some slight re-weighting within industrials – the sector it’s expected to land in – and Anthropic and OpenAI will bump up the tech sector weight a touch. Assuming 10% of shares are available to the public – a stretch given that the funding SpaceX seeks would require roughly a 4% float – a $2 trillion valuation for SpaceX, and $1 trillion valuation for Anthropic and OpenAI, tech’s weighting may rise by 10 bps. Industrials’ share could likewise rise by roughly 30 bps with financials, communications, discretionary and health care shedding about 10 bps of weight. SpaceX would be about the 5th largest stock by weight in industrials and assuming its valuation holds, SpaceX would need to get to just north of a 20% float though to be the largest company in that sector. However, at that float, OpenAI and Anthropic would enter tech as the 32nd and 33rd largest companies, commanding just a 0.4% weighting in the sector each.

Key to Watch – The Fed Could Extend the IPO Wave

Monetary policy might be key to extending the ongoing IPO cycle beyond the bulky issues that will come to market in 2026. While pre-pandemic, the relationship between rates and issuance was unclear, companies have gone public with greater frequency when monetary policy was supportive. Ahead of the 1999-2000 and 2007 peaks in issuance, rates were rising. But the return to zero interest rate policy (ZIRP) and quantitative easing (QE) in 2020 very clearly drove a surge in IPOs that lasted through 2021 and only ended roughly coincident to the Fed’s first rate hike in 1Q22. Those hikes then drove one of the weakest IPO cycles on record (rivaling the 2008 lows) that only began to reverse with the first rate cut in 3Q24. An easier path for interest rates could help grease the runway for more IPOs in 2027, but if the Fed is forced to hike with inflation pressures emerging from the middle east, they may just stop the IPO wave in its tracks.

Disclosure: HB Wealth is an SEC registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.