Abstract:

- Presumptive incoming Fed Chair Kevin Warsh’s testimony provided insight into major changes he would like to implement at the central bank. These include conducting monetary policy via rates instead of with the balance sheet, utilizing new measures of inflation, and altering the way the Fed communicates policy to the public.

- Removing the balance sheet from the Fed’s toolbox may be the change that could be met with the most uncertainty. Periods of quantitative easing and tightening have typically overlapped with rate policy. Balance sheet changes have been especially important to small caps.

- New inflation benchmarks might be deemed politicization on the surface but may help the central bank counteract asset price bubbles ahead of time. In the 1990s, early 2000’s and 2021-22 the trimmed mean measures that Warsh favors would have hinted at hotter than headline inflation or confirmed broad inflation pressures.

- The market’s reaction to changes in communications from the Fed is uncertain and depends on the extent of the rollback. Loss of forecasts from the central bank might sting markets accustomed to visibility.

Monetary Policy Faces Three Big Changes with New Fed Chair

With a new Chair calling for “regime change” on deck and the FOMC already on a relatively uncertain hold pending impacts from the war in the Middle East, monetary policy may be set to keep markets somewhat on edge for the remainder of 2026 and into 2027. The presumptive new Fed Chair, Kevin Warsh, has made his desire for reform clear. He sees the Fed as having lost credibility with markets and the public and argues that restoring that will require major structural changes. While the changes may not happen immediately given the need for approval from the 12-person FOMC, the prospect for major overhaul is at the very least likely to infuse a degree of uncertainty in markets. Warsh wants “a new framework, new tools, and new communications.” This may mean three large shifts as the new Chair takes the helm of the Fed; (1) The Balance Sheet is Out, Rates are In, (2) New Inflation Benchmarks are Coming, and (3) An End to Fed Forecasts (RIP, Dot-Plot).

Reviews Aren’t Unusual, the Sense of Urgency May Be

Periodic reviews of the Fed’s monetary policy framework are not particularly unusual. On average every five years, framework reviews have occurred through an official assessment and update of the FOMC’s “Statement on Longer-Run Goals and Monetary Policy Strategy”. However, Warsh invokes a sense of urgency for review that is unusual. The results of the last review were just announced in August 2025. Prior to that, a new statement was issued in 2020. So, anything announced before 2030 will break with recent precedent.

The degree of potential change may also be significant. The 2020 announcement was the last to make waves for markets. Back then, the Fed shifted to flexible average inflation targeting. This was intended to allow inflation to moderately exceed 2% after periods of undershooting, emphasizing inclusive employment as priority, but was considered by some (incoming chair included) as a major error. Given the 2020 policy shift has been blamed for the surge in inflation over subsequent years, markets may be rather anxious about significant inflation benchmark changes emerging with the Warsh-led Fed.

Nonetheless, we see three primary issues to watch with respect to a potential Fed policymaking framework overhaul:

(1) QE is Out, Rates are In, and a Treasury-Fed Accord is on the Table

Shrinking the size of the Fed balance sheet appears to be a key pillar to Warsh’s strategy for reforming the Fed. He has argued for a Treasury-Fed accord to shrink the size of the balance sheet, getting the Fed out of practicing what he sees as “fiscal policy in disguise”. Broadly, this may mean a Fed that looks a lot more like the pre-financial crisis Fed, shifting the composition of its balance sheet to much shorter duration. He wants rate cuts and balance sheet reduction happening in parallel, with cuts aiding the real economy as balance sheet reduction limits asset price inflation.

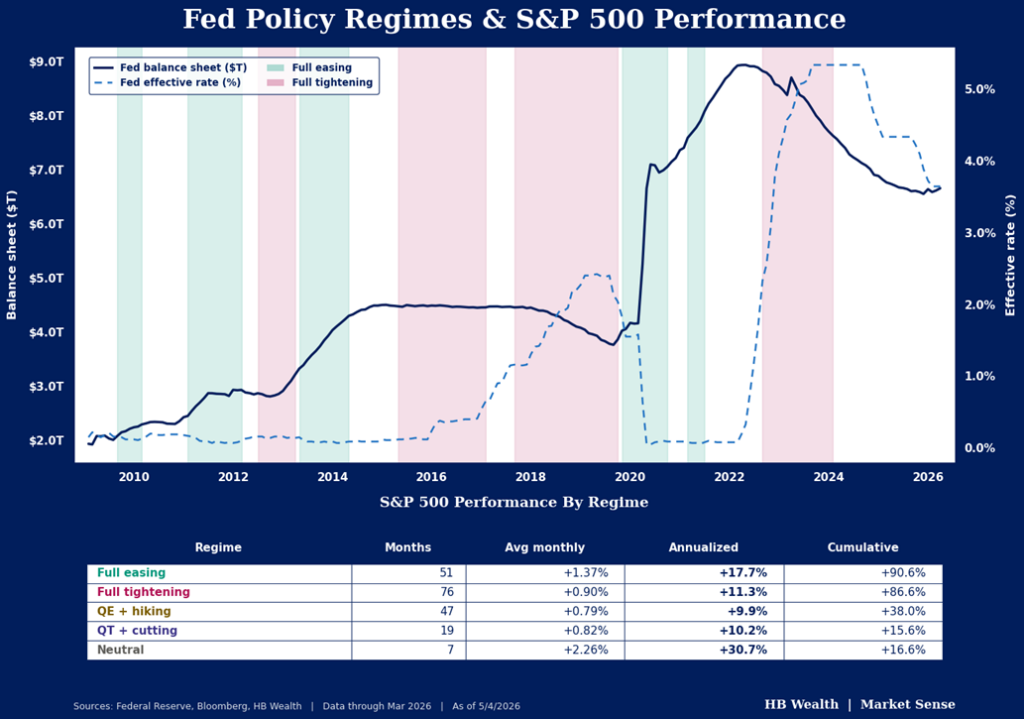

This could be the most impactful change for financial markets to absorb, for the balance sheet has been a key pillar of monetary policy making since the Great Financial Crisis (GFC). Across the economic cycles since then, periods of expansion and contraction in the balance sheet accompanied large shifts in equity valuations due to impacts on rates. Quantitative easing (QE), combined with rate cuts flipped real rates to negative in 2012 and 2021, causing abnormally high equity risk premiums and hinting that stocks were cheap. Likewise, quantitative tightening (QT), first in 2018 and more dramatically from 2022-25 caused the opposite. Stocks now look the most expensive relative to bonds since the dot-com era – see Warsh Fed Could Spell Trouble for Already Tight Equity Risk Premium – HB Wealth.

Warsh’s proposal to shrink the balance sheet while continuing to lower rates could likewise alter equity returns. The average annual price return for the S&P 500 in the 16 years of the balance sheet era is 13.5%, versus 6.6% during the prior 16 years. Periods of fully neutral policy have been rather rare since 2008, as the market has had to contend with extraordinarily persistent intervention from the Fed. The Fed has most often been double easing or double tightening – implementing policy with the balance sheet and rate cuts in tandem. Most rate cut periods since the GFC coincided with balance sheet QE, and stocks returned an annualized 17.7% in those cycles. Opposing Fed policies might confuse the market and add uncertainty about policy goals. In regimes where the Fed was paring back the balance sheet but cutting, the S&P 500 gained an annualized 10.2% — those observations largely occurred during the most recent rate-cut cycle that started in late 2024.

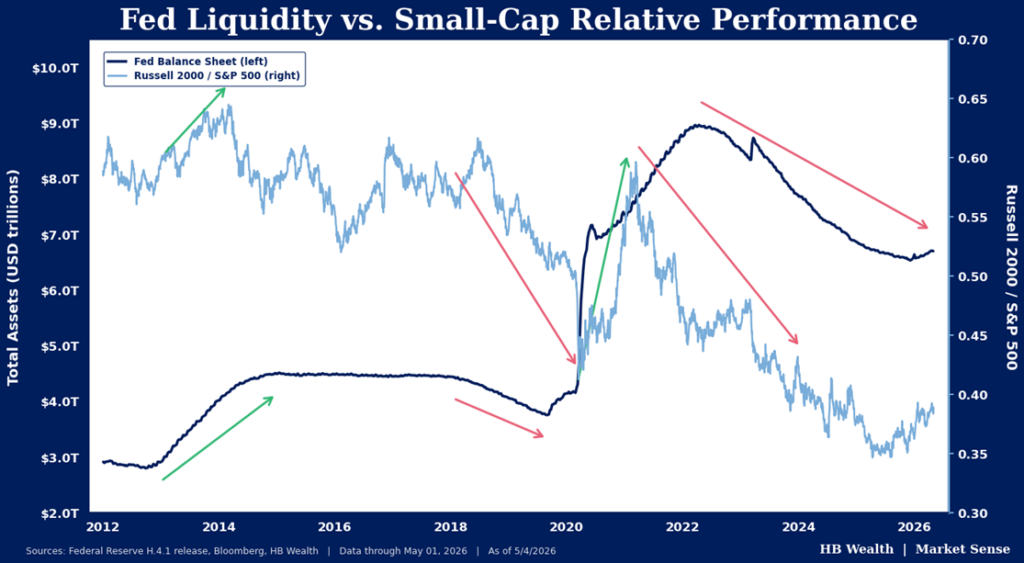

Small cap stocks may feel the impact of a balance sheet unwind most, unless it is accompanied by substantial lowering of the policy rate. The balance sheet has shown a strong link to small versus large cap relative performance since the GFC, with periods of quantitative easing generally supporting Russell 2000 outperformance, and vice versa. The onset of QE3 in late 2012 coincided with a 2-year stretch of small cap outperformance, for example, and the Fed’s massive infusion of liquidity in 2020 helped small caps lead by a whopping 72.9 percentage points over the next year, ultimately culminating in an asset price bubble centered on unprofitable health care stocks and the sudden rise of SPACs. Conversely, the first QT cycle, starting at the beginning of 2018 and lasting into late-2019 helped small caps lag the S&P 500. Likewise, the latest bout of tightening (from 2022-2025) accompanied a 35.5 percentage point lag for small caps.

(2) Core PCE is Out, Real Time Data is In.

As policymaking becomes more dependent on rates and less reliant on the Fed’s balance sheet, key metrics for determining policy direction are also likely to get a refresh with the new Chair. Specifically, favored inflation benchmarks appear to be up for debate. As we reviewed above, the FOMC attempted to alter the inflation assessment with 2020’s framework announcement, and that did not go over particularly well. Thus, a shift in how the Fed views inflation should not be underestimated for its potential impact on financial market outcomes.

In the recent past, the Fed has relied heavily on core PCE as its primary benchmark. While they take into account several different measures of inflation, the PCE price index has generally been the Federal Reserve’s preferred inflation measure since 2000. However, on account of his assessment of Fed policy failure in the 2021-2022 inflation experience, Warsh has proposed an alternative approach to understanding inflation. This means markets’ traditional benchmarks for inflation are up for debate. He has suggested a preference for developing a “billion-prices survey” to capture inflation rather than headline noise, and that trimmed mean and real-time data could become the Fed’s primary lens on inflation rather than PCE.

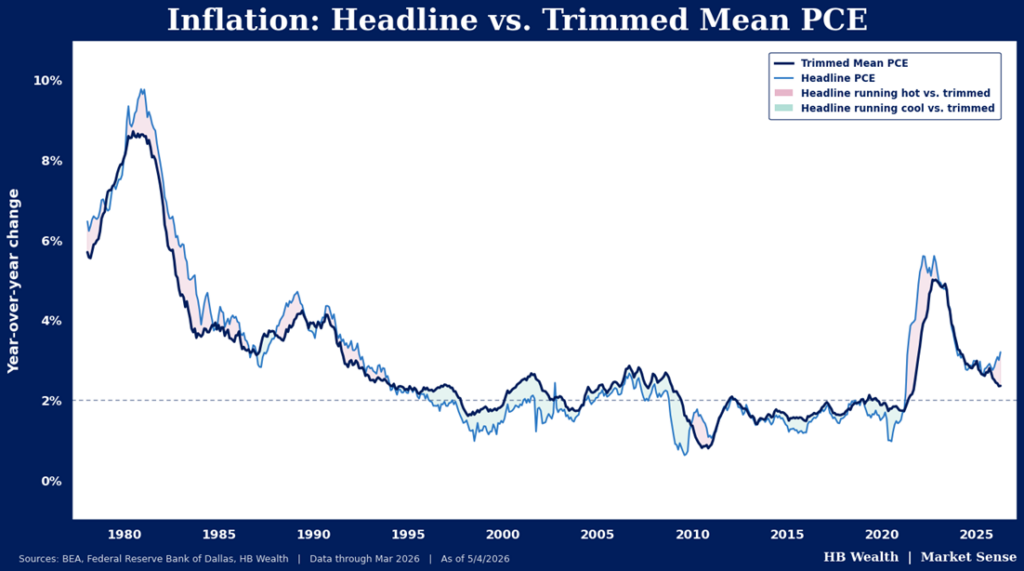

The trimmed mean version of PCE is likely to face the most pushback from pundits and economists alike given the current level of politicization around the Fed – but that critique might be a bit myopic. While the trimmed mean perspective supports cuts now, it would have pointed to much tighter policy in the lead up to both the 2000 tech-bubble peak as well as the housing-bubble peak in 2008 and thus may have helped prevent excessive risk-taking in each period.

The Dallas Fed’s trimmed mean PCE measure of inflation clips the top 31% and bottom 24% of PCE components by their price change instead of removing food and energy costs to offer a measure of core price pressures. It currently suggests the U.S. economy is in a more disinflationary environment than the traditional core PCE, at 2.4% versus 3.2%. While this is still above the target rate of 2%, it may imply an easier bar for near term rate cuts and provide a convenient excuse to do the President’s bidding. Yet, this inflation perspective may also have resulted in tighter Fed policy in the lead up to both the dot-com bubble and GFC, when the trimmed mean measure suggested slightly more price pressure than evident in Core PCE. Likewise, a look at trimmed mean inflation may have helped dispel notions that inflation was “transitory” in 2021-22 as it confirmed the rise in traditional measures of core inflation.

(3) Back to a Black Box? Dissent Encouraged

For decades, the Fed has been accelerating communications in an attempt to open the blackbox of policymaking for the markets. That could change materially under the new chair. Warsh would like to abandon forward guidance, which he believes constrains policymaking flexibility, and he has declined to commit to continuing with regular post-meeting press conferences, which the Fed has held since the financial crisis. He also may consider reducing the number of policy meetings per year, a break from the eight-meeting annual cadence in place since the 1980s.

It is highly unclear how much a cut in communications could impact markets given it is a somewhat unprecedented pivot for the Fed, but we suspect the degree to which lesser communications might increase volatility will likely depend on how much communication is cut from the Fed’s agenda. Prior to 1994, the Fed did not announce FOMC rate decisions until weeks after they were made, so market participants were forced to derive central bank policy from market moves. Then Chair Greenspan decided to publicize the decision to hike rates for the first time in 5 years as he felt such an unexpected change in policy could roil markets. This shift in communicating policy decisions expanded over subsequent decades to include substantially more timely analysis and information from the Fed. It is unlikely that Warsh would want to roll back all of these communications. It instead seems likely that he might focus on limiting the Chair’s press conferences – which Bernanke instituted with a quarterly cadence, and Powell eventually accelerated to 8 times a year. Those have been observed to drive some volatility in themselves as investors juxtapose commentary with the FOMC decision.

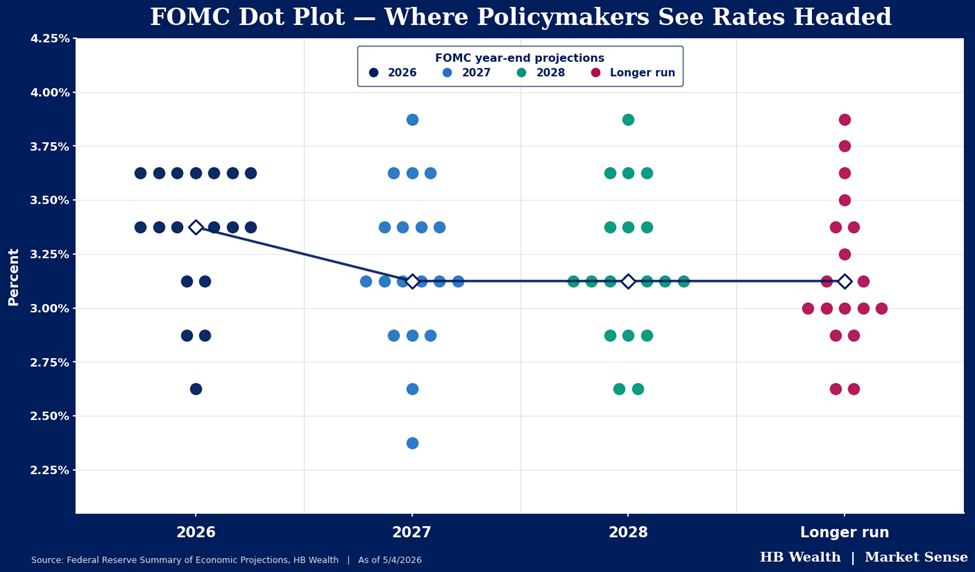

The presumptive Chair also expresses dislike for forward guidance, suggesting the beloved dot-plot may become of thing-of-the-past under Kevin Warsh. The dots have been around since 2012 and are one of a sequence of communications enhancements included in the Fed’s summary of economic projections (SEP), in place since 2007.

The FOMC first announced the increased frequency and expansion of the content of economic projections released to the public in 2007, and the Fed has persistently added more data and context to the projections in the years since. Compared with projections previously released semiannually, the quarterly SEP has a longer forecast horizon and includes projections for headline PCE inflation. It also includes forecast errors of various projections made in the past. Participants’ assumptions about the appropriate level of the federal funds rate at year-ends and in the longer run (the dot plot) was added to the SEP in 2012.

In addition to the changes in external communications, it seems the internal dynamics of policy meeting discussions may shift as well. Warsh has stated a preference for genuine dissent, in contrast to very limited voter dissent under Powell’s tenure. It is unclear whether markets will be able to observe and analyze this dissention in FOMC discussions. To us, it seems a shame the Fed’s communications may be set to roll back, just as the meetings may be about to get even more interesting.

Disclosure: HB Wealth is an SEC registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.