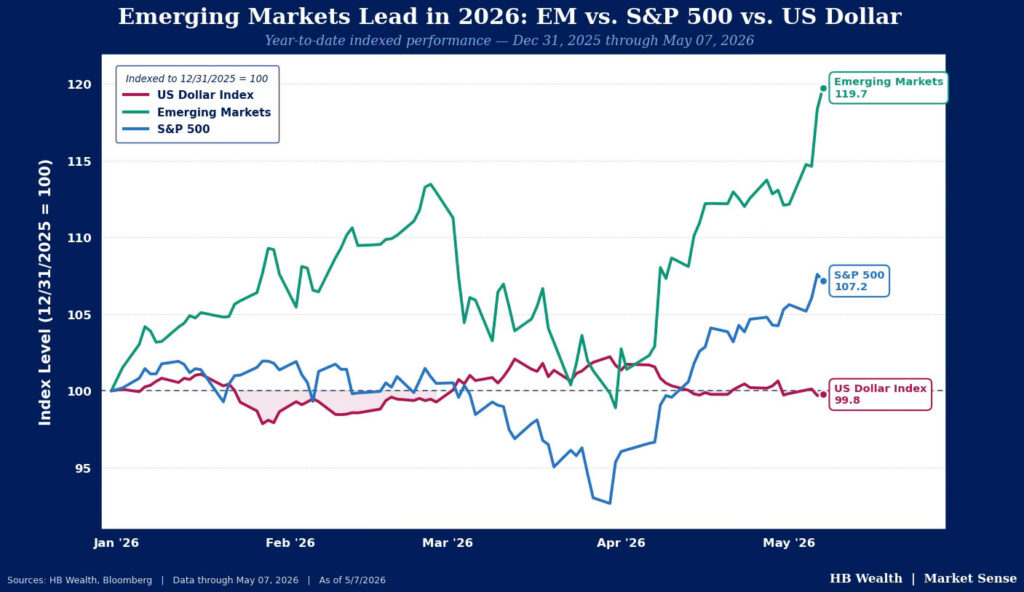

Emerging Market equities are on pace for a second consecutive year of outperforming U.S. stocks, the first back-to-back annual outperformance since 2010. So far this year, the group has outperformed U.S. large caps by more than 2X, up nearly 20% versus the S&P 500’s gain of 7%.

Notably, emerging market equities have risen without valuation expansion – the group has only gotten cheaper this year, and forward P/E is just 12X thanks to consensus estimates for very strong EPS growth over the next year. This compares to the S&P 500’s 21X and offers considerable cushion for any downward adjustments to expectations that may occur if war in the Middle East becomes a bigger issue for earnings growth. The group has also not gotten any support from the dollar, which has gone nowhere for six months.

Of the dozen largest emerging markets, half are outperforming the U.S. while half are underperforming. Korea and Taiwan are in the lead given tech concentration, while Brazil, Thailand, Columbia and Peru are all also outperforming U.S. stocks. Heavyweights China and India have lagged the U.S. Sector cross currents are similar to those facing domestic stocks – for the year tech (up 64.8%) and industrials (up 29.1%) are leading with AI-heavyweights Taiwan Semiconductor, Samsung Electronics and SK Hynix among the largest contributors to EM returns.

Disclosure: HB Wealth is an SECregistered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.