It is no secret that private credit redemptions are rising as concerns about default risk hamper performance of this most beloved asset class. As the “Golden Age” of private credit normalizes, we may continue to see liquidity pressures rise and questions about underlying loan valuations emerge. As financial markets remain on guard for signs of eroding credit quality, spreads and equities can shed some light on contagion risks. So far public market spreads remain quite calm, but equities are wobbly, with BDCs struggling and insurance stocks showing some anxiety.

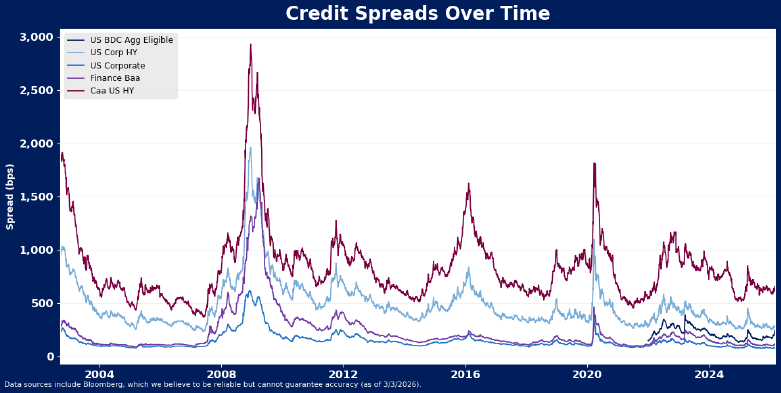

Credit Spreads Suggest Little Concern

Credit spreads offer a lens on the broader markets’ interpretation of credit quality and default risk, and across the board show no sign of material deterioration. While off their tightest levels reached in early 2025, even the lowest quality high yield bond spreads are still very tight compared to other periods of stress. Last year, when tariff policy was emerging, Caa spreads touched 850 bps, still well above the current level of 628 bps. On average, Caa spreads rose 584 bps in mid-cycle corrections like 2011, 2015, 2018, and 2022, and touched at least 1000 basis points in each instance.

Even Bloomberg Aggregate-eligible BDC credit spreads, arguably closest among categories to the private credit market, appear remarkably contained at this time. This aggregate has limited history, but at its peak in March 2023, the BDC spread touched 387 bps. Currently the spread of 251 bps is about equivalent to the spread touched in 2025.

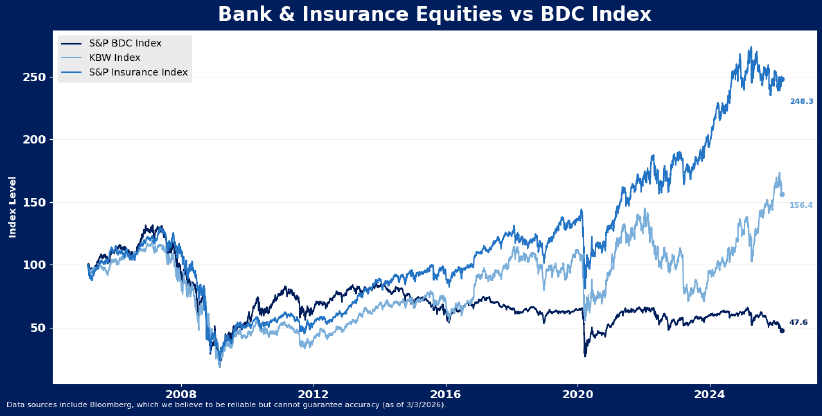

Watch Banks and Insurance Stocks for Contagion Risk

Equity markets appear a bit more concerned than credit markets. BDCs, arguably a public market canary in the private credit coal mine, have taken a significant dive in recent months. Also, while there appears little sign of concern that strains from private credit will erode performance of banks, insurance companies are struggling a bit. History suggests both groups will likely sell off significantly if a broader risk of contagion emerges.

BDC equities (the S&P BDC index includes Ares, Bain Capital, Blackstone, Blue Owl, etc.) have struggled with a 23.7% decline from recent peak reached in July 2025 and are now trading below 2022 levels. Intriguingly, BDCs have been in a long-term bear market that dates back to the index peak prior to the financial crisis. The equities recovered to a post crisis peak in 2013 and struggled since then. Public BDCs are capital constrained as they cannot issue equity when their stock is below book value. The strong flows into direct lending have largely come through private BDCs as they can raise nearly unlimited amounts of capital. Nonetheless, the recent decline in equity values and increasing discount to NAV in public BDCs is likely partly due to an expected rise in defaults for the industry.

Movements in the value of BDCs usually coincide with movements in bank and insurance stocks as perceptions about default risk flow through to portfolio asset valuations. Concerns about private credit markets are so far dimming optimism in insurance companies but are not impacting the banking sector as much. Banks, represented by the KBW index, are down 10% from their peak in early February, but just back to levels last recorded in December. The group is still up more than 15% compared to this time last year. Insurance stocks, represented by the S&P Insurance Index, have dropped 10% from their peak in April 2025, and are down 7.2% from a year ago.

Notably, in the years prior to the financial crisis, banks, insurance and BDCs were very tightly correlated. The correlation between banks, BDCs, and insurance companies and BDCs averaged 0.88 in the three years before the financial crisis. The correlation has been nearly cut in half in the post-pandemic era. If private credit risk becomes a broader systemic risk, a tighter correlation should emerge.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.