Abstract:

- S&P 500 1Q EPS Reporting Season Starts This Week

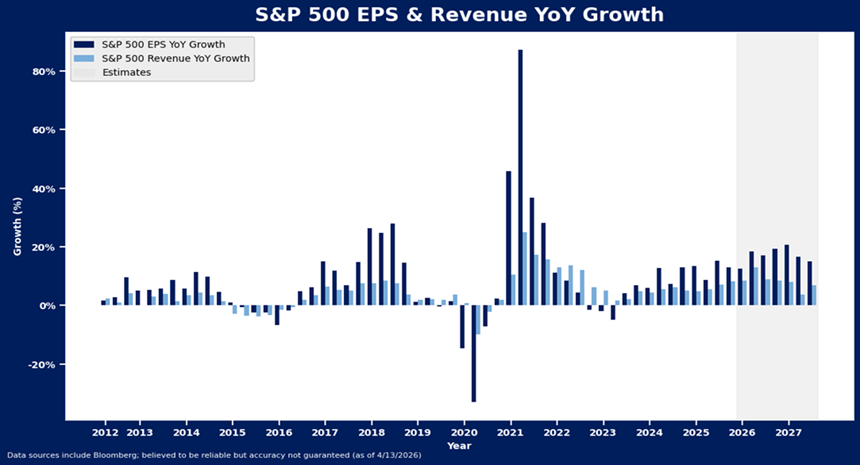

- Analysts expect 12.8% YoY Growth vs 13.4% in 1Q25

- Watch Revisions, Margins, and Technology Sector as Keys this Quarter

S&P 500 earnings face high hurdles this earnings season but given the ongoing conflict in Iran and the drastic effects that AI-spending could have on free cash flow, success in 1Q will be much more about guidance and the forward outlook than clearing consensus expectations. Operating margins and their forecasts for the rest of 2026 will likely be the income statement item to watch with consensus already trimming estimates across consumer discretionary, staples and industrials. Likewise, AI related capex is propelling tech’s rapid profit growth but perceived lack of return on investment at the individual company level might drive volatility in results. Broadly, the index will need to live up to expectations for very robust earnings to continue into the second half of this year to keep stock prices moving in a positive direction.

Three Keys to Watch in Earnings Season

The S&P 500 earnings season kicks off this week, with the companies facing lofty expectations that must be hurdled to keep stock price momentum in the green as we enter a second week of tenuous ceasefire in the Middle East. Analysts are currently forecasting 12.8% YoY EPS growth for S&P 500 companies in 1Q26, on par with the 12.9% recorded in 4Q25. Last year, the index recorded 13.4% growth.

We are watching three keys to earnings season this quarter. First, the backwards-looking nature of results, earnings this quarter won’t tell the full story. Investors will likely be watching for positive revisions and guidance as the true signpost for success. Likewise, companies will have to show operating margin resilience in the face of rising input costs to satiate investors. Finally, tech’s (and especially the software industry’s) earnings and cash flows will remain under the microscope.

Revisions and Guidance to Reveal Extent of War-Resilience

Past results may offer only limited perspective on corporate earnings trends given the new pressures that emerged with war in the month of March, suggesting forward estimate revisions and guidance may offer the most market-relevant information this quarter. Analysts have started marking down estimates for 2026 growth in the most commodity price sensitive areas of the index so far. Consumer discretionary and industrials estimates are down most, but adjustments are so far offset by surging expectations for energy sector growth. Guidance on the 1Q earnings season has skewed negatively, but very few companies have offered guidance for 2Q earnings to date, and the distribution is split between positive and negative adjustments.

Margins May Make or Break the Outlook

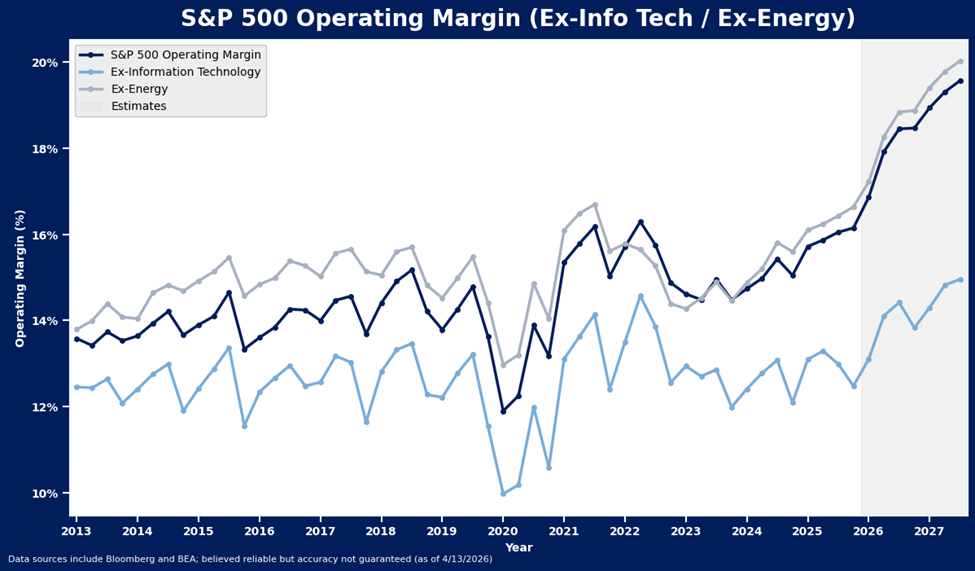

The conflict in Iran is driving some supply chain stress that, combined with pre-war signals of rising input cost pressures, suggests margins are likely to be scrutinized heavily in the upcoming reporting season. Ex-energy operating margins should be particularly key. Currently the consensus is anticipating a significant rise in ex-energy operating margins, to 17.2% from 16.1% a year ago in 1Q, with further gains to new highs through 2027. This is mostly thanks to the technology sector, and semiconductors especially. Consumer discretionary, staples and industrials operating margins are all expected to drop in 1Q relative to a year ago but then show rapid recovery after that. By the end of the year margins ex-tech are expected to hit new highs, in a sharply positive turn higher after years of sideways churn.

While consumer stocks’ exposure to high oil prices is well understood, AI-related infrastructure plays may also face some underappreciated risk of margin squeeze from the sudden shift higher in input costs. Construction & engineering companies that are tasked with building data centers may lack pricing power to push higher energy costs onto big tech. In contrast, utilities – which have been riding the AI-buildout wave – could be spared as disruptions in the natural gas market didn’t spread to the US given abundant domestic production. Gas accounts for 43.1% of domestic electricity generation according to the EIA, and Henry Hub prices have fallen throughout the Iran conflict.

Tech Remains S&P 500’s Growth Engine but Software Risks Persist

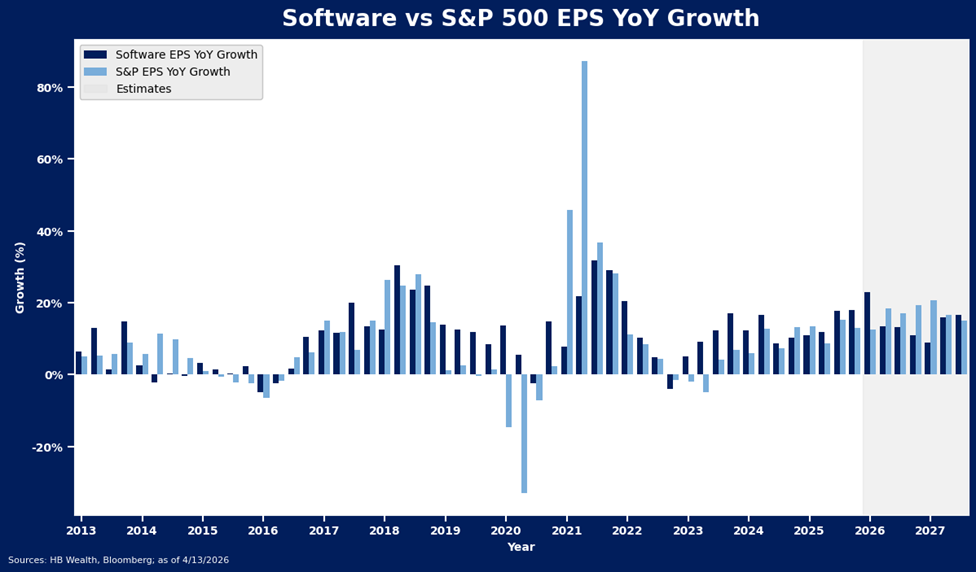

Tech is expected to lead the charge among sectors with 39.3% YoY EPS growth in 1Q, but earnings details from the software & services segment may set the tone. The group is expected to be a relatively weak link in the sector, with just 13.4% growth, down from 23% in the prior quarter. Earnings are expected to continue to decelerate toward single digit growth by the end of the year.

Yet, the biggest risk to software doesn’t come from near-term earnings. Investors are both actively reassessing the seat model and scanning the industry for companies with significant moats as AI threatens to displace white collar workers and lower barriers to entry to building new software. Thus, a repricing of terminal value is currently underway with investors looking to make bets on the survival of many of these companies – driving a wedge between current multiples and typical cash flow measures of value.

Meanwhile, the S&P 500 mega-cap hyperscalers will likely need to walk something of a tightrope that is not too hot nor too cold on capex. Stability, but also no slowdown in spending plans may be needed to show the group can stabilize free cash flow. AI-hyperscalers have already seen free cash flow (FCF) generation slip to levels akin to 2022’s bear market.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.