Even if the recent spike in commodity costs proves fleeting, a secular reality of higher average inflation with large spikes may be setting in, and this may be tricky for stocks to shrug off, particularly at current valuation levels. The bond market’s implied inflation expectations for the next year have surged beyond 5%, the highest level since 2022, and forecasts for longer term inflation are on the rise as well. If the bond market proves correct, U.S. stocks may face valuation pressure in the short run – S&P 500 P/E is still over 23X but averaged less than 13X in past periods when inflation was over 5%.

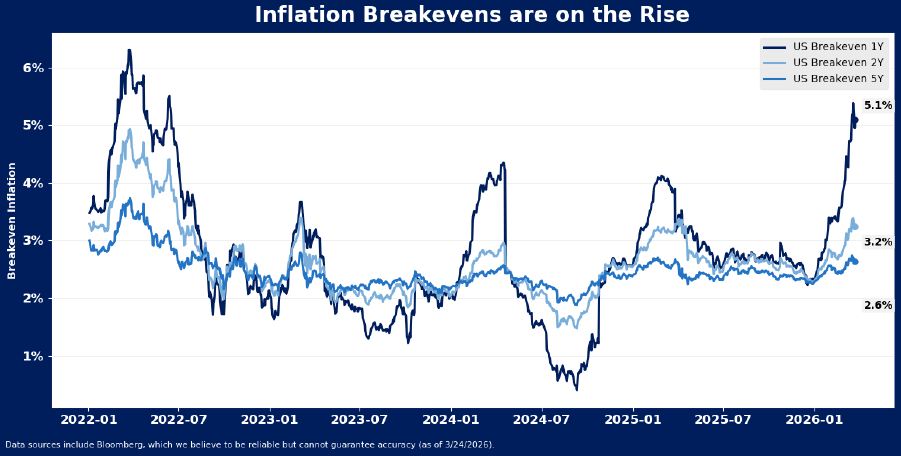

Inflation Expectations Resetting Across Time Horizons

Bond markets have rapidly repriced near-term expectations for U.S. inflation in response to surging commodity prices. The implied 1-year breakeven inflation rate is now above 5% for the first time since 2022. Back then, the implied inflation rate broke above 6% at its peak and held north of 4% for over 14 weeks. So far this time, the 1-year inflation expectation has been above 4% for just 3 weeks.

The jump in near term inflation has also pushed forecasts for 2 and 5-year breakevens higher, though both longer-term tenors remain more contained than they were in 2022. The 2-year inflation outlook is now 3.3%, and the 5-year outlook is 2.6%, according to the bond market. These rates have been rising since the end of 2025, but have jumped recently, also likely reflecting the near-term spike in commodity costs.

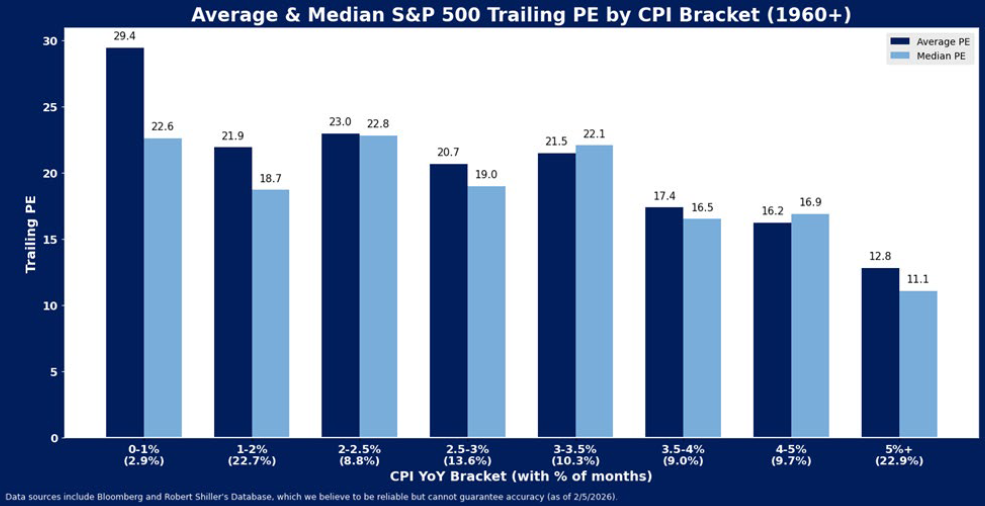

Valuations Do Not Fare Well with Inflation Over 3.5%

Elevated bond market-implied inflation expectations may present a problem for U.S. large cap equity valuations because the market is priced to expect very little inflation at this time. Currently the S&P 500 is trading over 23X times trailing earnings. On average historically, P/E managed to average a level over 20X only when inflation was below 3.5%. The S&P 500 P/E averaged closer to 17X when inflation was between 3.5-4%, and that average dropped to merely 12.8X when inflation accelerated past 5%, historically.

Inflation is so far predominantly a reflection of high commodity prices that may be resolved with a wind-down of war in the Middle East and opening of the Strait of Hormuz. Thus, the equity market may continue to dismiss the budding inflation problem as a temporary bond market overreaction. In 2022, inflation risks were also perceived to be transitory…until they weren’t…and then were again. This makes the bar even higher for markets to adjust expectations this time around.

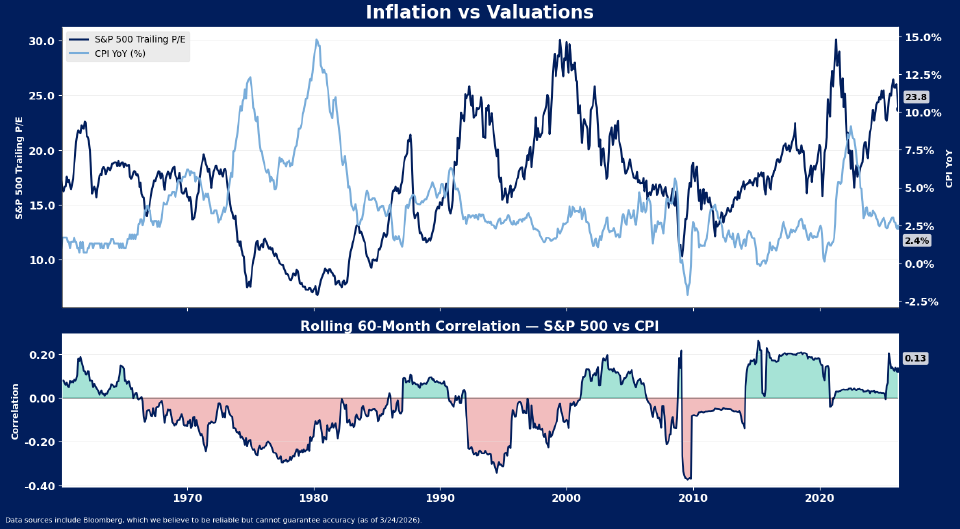

To shift the market perspective on inflation, the long-term correlation between market valuations and inflation may need to signal a more permanent change. Since just after the financial crisis, the correlation between PE and CPI has been positive. Equity valuations and CPI have moved in tandem as nearly all of the increases in inflation were considered positive indications of rising demand. That has not always been the case. For most of market history before the financial crisis, CPI and PE were inversely correlated. A return to negative correlation between inflation and equity valuations will likely signal a more permanent shift in inflation sentiment has emerged.

Persistent inflation is perceived to be a phenomenon of the past in the U.S., and as a result the equity market is prone to believe inflation spikes are likely to be fleeting. Thus, the market may continue to shrug off this latest inflation spike as temporary in nature. However, it should not go without notice that inflation spikes have been more frequent and at higher levels this decade. We are currently experiencing the second spike in expectations in three years, a phenomenon last recorded more than 40 years ago. Meanwhile, consumer price inflation has been holding above 2% since the pandemic, something that hasn’t happened since the late 1980s. These signals send a warning shot to financial markets that may be ill-prepared for a different inflation regime. The more shocks accumulate, the less the equity market’s sanguine interpretation of inflation reflects reality. Amid rising inflation risks, equity valuations look increasingly out of bounds.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.