Abstract:

- Semiconductors are one of the largest groups by market cap in the S&P 500 and offer a look at risk appetite for the index at large given their central role in the global AI-buildout.

- The group’s parabolic move of more than 50% over the last six weeks sets a rocky backdrop for the market at large, particularly given prices have advanced much faster than earnings. Valuations show expectations will need to be met and likely exceeded for the group to perform well.

- We identify three fundamental issues to monitor for the bull market in semiconductors: hyperscaler spending plans, the competitive landscape, and policy risks.

One of the largest, risk-tolerance-setting industries in the S&P 500 – semiconductors – has jumped more than 50% from March low to last week’s high as earnings continue to blow past consensus. Technicals may already be in the process of correcting but remain only part of the concern. Valuations based on the past are well beyond former peaks while future-based multiples remain within range of norms, suggesting the market is largely banking on soaring growth to continue. Thus, one of the market’s largest risks may arise if semiconductor stocks are unable to substantiate sky high expectations. Stress is not assured but could come from one of three primary areas – hyperscalers start to scale back spending, new AI-model developments require less compute than already built, or political winds shift to disfavor this large and leading industry in the S&P 500.

Earnings Optimism is Keeping Semis, and the Market, Afloat

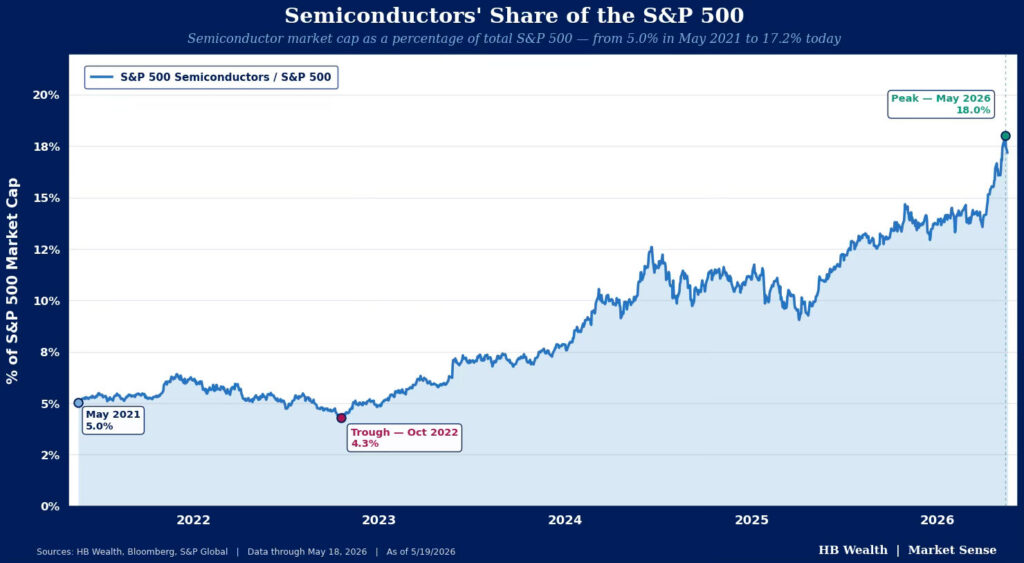

Semiconductor stocks have historically set a strong precedent for the tone in markets, but do so now more than ever, given their size and leading role in the AI revolution. This group is more than 17% of the market cap of the S&P 500 – that’s more than double their share of the index at the peak of the tech bubble in 2000. These stocks have risen at a rarely recorded parabolic pace – up more than 50% over the six weeks ending last week, and accounting for a whopping 39.5% of the index’s gain since the March 30th low. Semiconductors added 6.6 percentage points to the S&P 500’s rise in that time — nearly 3x the contribution of the next largest industry contributor to the index gain (interactive media, which includes Alphabet and Meta, among others).

Earnings have helped spark the recent optimism for the group, but only partly justified the rapid escalation in price, suggesting the group is dependent upon continued advances in expectations to justify future price moves. Over the last five years, the SOX (Philadelphia Semiconductor Index) price has jumped 296% versus the actual earnings rise of 84%. Price growth has also surpassed the gain in earnings expectations by a wide margin, even though analysts are expecting semiconductors to remain one of the strongest growth engines of the index in the year ahead, with anticipated net income growth of 59% on a revenue gain of 31% in 2027.

Semis Multiples — Average at Best, Bubble at Worst

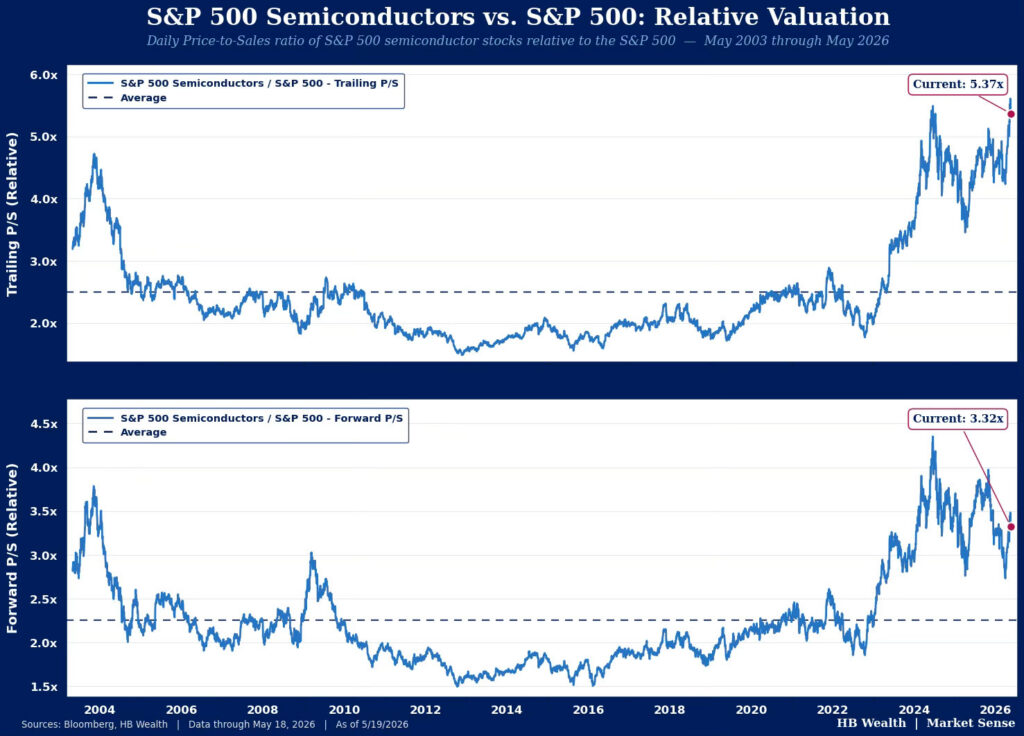

No matter how you slice the group, it’s no longer cheap, and given high embedded expectations, significant multiple expansion may be tough to come by for semiconductors. The group trades at 19.6x trailing sales – the highest multiple the group has ever commanded, surpassing the 17.6x high from October and good for 2.4 standard deviations above the 5-year norm. Meanwhile, it’s at 11.1x forward sales, still below October’s 13.2x apex, but nonetheless 1.3 standard deviations above recent average. The difference between the two lies in forward estimates – semis is pegged for average 57.3% revenue growth from 2Q26-1Q27. Even relative to the S&P 500, semis is 1.8 and 0.7 standard deviations expensive on a trailing and forward basis, respectively, and has been commanding a premium north of the 2000 apex consistently since late-2025.

Likewise, a similar story emerges among earnings-based multiples. On a trailing basis, semi’s 50.4x multiple is 1.7 standard deviations above 5-year average with last week’s high setting a new apex for absolute multiples outside of the dot-com era (when they got to a whopping 118x). The group’s forward multiple falls to 23.5x as a result of an average 87% earnings surge from 2Q26-1Q27 but that’s smack on the recent norm. Only on a forward basis relative to the S&P 500 does even a slight discount (0.4 deviations below 5-year average) emerge.

Estimates are Great, But If Hyperscalers Catch a Cold Then Semis Get the Flu

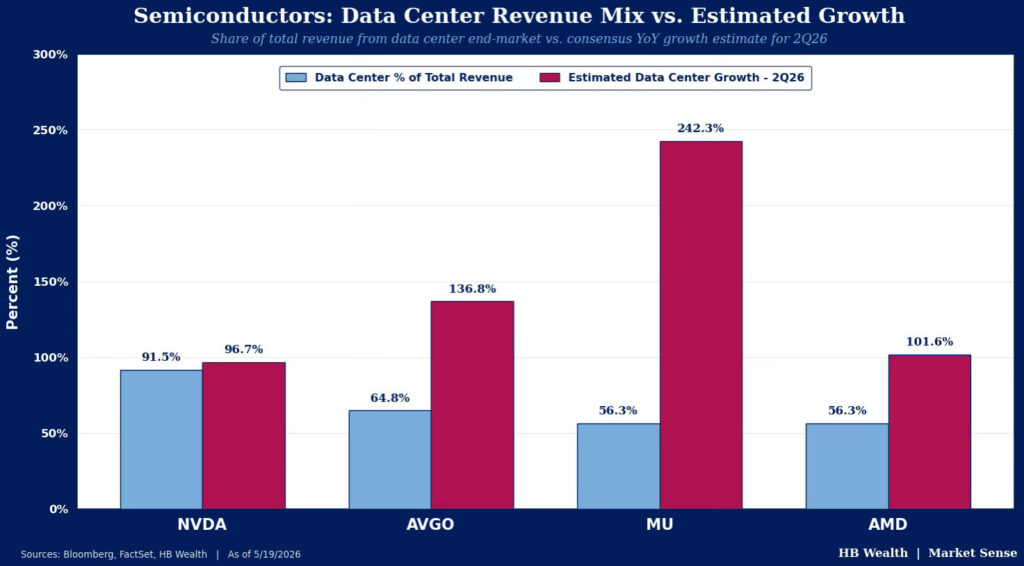

With valuations still reasonable based on robust forward forecasts, but extreme based on the past, the future for semiconductors will likely largely depend on the predominant driver of revenue for the group, and that’s hyperscalers’ continued willingness to spend. Estimates for hyperscaler capex are already expected to push over $1 trillion in by 2027 (see our Deep Dive here) and semis have been the largest beneficiary of that spending. Across the five largest semiconductor companies – Nvidia, Broadcom, Micron, AMD and Intel – data center segment revenues were an average 61.2% of the total as of each stock’s last reported quarter. Likewise, analysts estimate average 144% data center revenue growth across the four companies (Intel doesn’t have an estimate for data center revenues) in 2Q26, led by Micron (242.3%) and Broadcom (136.8%). Interestingly, Nvidia’s data center growth is expected to be slowest that quarter (up 96.7%).

Still, another possibly less foreseen risk to estimates remains – more efficient AI models that require substantially less compute than has been built. In January 2025, when DeepSeek released their R1 model, it caused a brief bear market in Nvidia stock and the semiconductor industry at large as investors questioned if such massive data center investment was necessary to train a more efficient AI model. However, it turned out DeepSeek’s model was trained using Nvidia chips and the stock quickly recovered. If significant efficiency gains can be made on the training side, it could translate to shrinking bookings as compute capacity outstrips demand.

Finally, government policy shifts have had significant impacts on the ebb and flow of semiconductors stock prices in recent years and can continue to do so given the importance of the industry for national security. Tariff implementations, export controls, and regulatory framework changes are all fair game as the administration strives to restore domestic production of semiconductors.

Disclosure: HB Wealth is an SECregistered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.