Abstract:

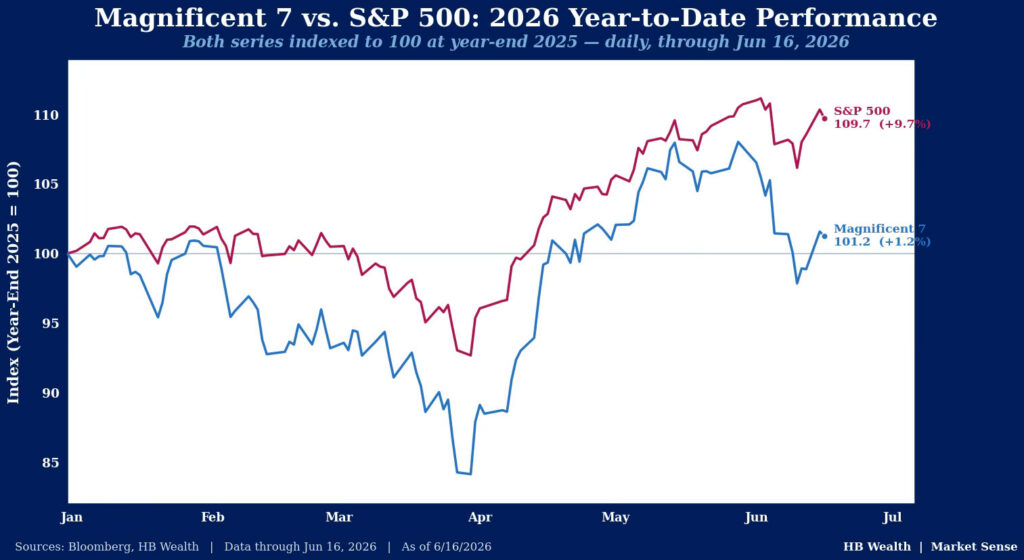

- The magnificent-7 has lost momentum since its May high as volatility around Nvidia and Broadcom’s earnings derailed the rally.

- However, both tech and the overall market have broadened with a wide swath of stocks picking up the slack from the mega-caps.

- A turn in economic indicators is driving an earnings resurgence for the other 493 S&P 500 stocks.

- Unlike 2022, the mag-7’s loss of leadership is due to the economy synching up and accelerating rather than disjointed earnings woes for various groups within the index.

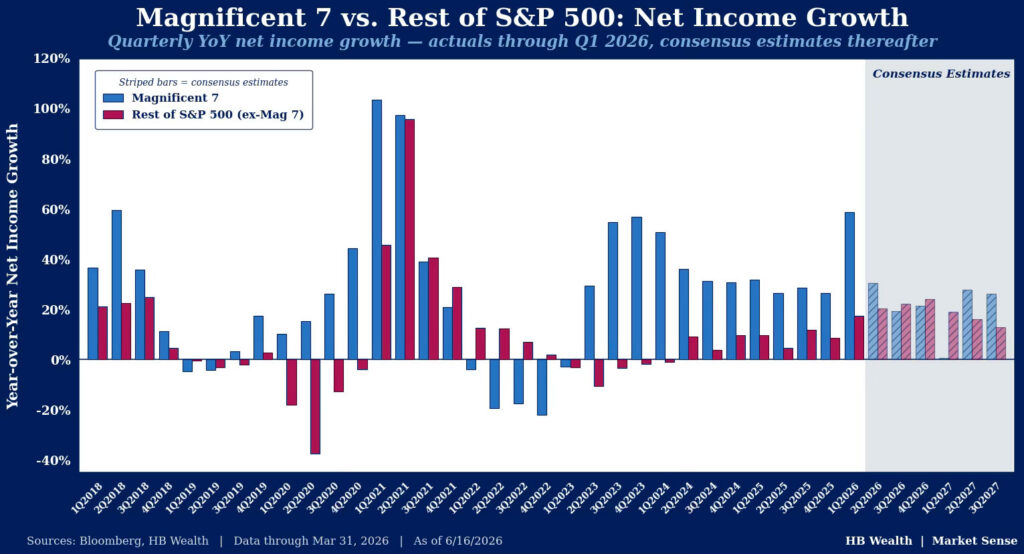

The Magnificent-7 has struggled relative to the rest of the market for most of this year, but unlike in 2022, the slowdown in this group is not taking down the market at large. If the consensus of Wall Street analysts is correct, 2Q could be the last quarter of earnings dominance for the cohort until mid-2027. The last time Mag-7 earnings struggled, it coincided with a bear market for the S&P 500. Back then, earnings for the group dropped YoY and the rest of the S&P 500 slowed down under pressure of high inflation and tightening Fed policy, exacerbating the market reaction as Mag-7 earnings faded. This time, Mag-7 growth is merely slowing, and is not likely to fall. Meanwhile, leading indicators suggest the economy is on firmer ground. With this earnings backdrop, the market could continue to weather a slowdown in Mag-7 earnings growth, and the rotation out of Mag-7 toward other areas of the equity market may continue to gather momentum.

The Mag-7 Hasn’t Been as Magnificent of Late, Rest of Tech Stole the Spotlight

The Mag-7 has given back over 7% since the group made a new high in May, and its relative performance versus the index is bouncing off support with the group’s June 15th rally. Performance initially started to weaken around Nvidia’s earnings, which saw shares sink despite a strong report as estimates were simply too high. Selling accelerated further with disappointing guidance from Broadcom. While that stock isn’t officially in the Mag-7, there’s a very good case that the cohort should make room for it – by market cap Broadcom is the sixth largest company in the S&P 500 and offers a key read on the AI trade. Nonetheless, earnings miscues coupled with nosebleed multiples have kept Mag-7 stocks constrained below their October 2025 relative performance peak.

The broad tech sector has held up better than the Mag-7, and is now up 11.2% from its high last October and has nearly doubled performance for the S&P 500 year to date. Since the March low, four of the six industries in tech are up more than 30% with software (up 13.1%) and IT services (up 1.8%) the exceptions. Likewise, the average stock in the sector has gained 46% (a median of 35.8%), showcasing the remarkable breadth across the sector that drove it to a new relative performance high. While the sector has dropped about 6% from the early-June high, both relative and absolute performance charts are holding near May’s supports.

As we’ve highlighted in our Market Sense here, the broadening trade hasn’t been limited to just tech. It’s occurring across capitalizations, factors and styles as the Mag-7 has taken a breather. While the Mag-7 at large is up only 1% so far this year, 61% of the S&P 500 stocks are up more than the Mag-7, and 42% of the index has gained more than 10%. Meanwhile, the Russell 2000 index of small cap stocks is up 18%, and 63% of its constituents have posted an advance in share prices this year.

Leadership Lost, Leadership Gained: Macro Elevates the 493

While the market’s struggle with the loss of Mag-7 leadership in 2022 helped result in a bear market (a loss of more than 20% peak to trough), that’s not the backdrop stocks have today. Unlike in 2021, when struggles of the Mag-7 were too large for the rest of the market to overcome given heavy inflation pressures and Fed tightening, the Mag-7 is losing leadership as the rest of the index appears to have a fundamental catalyst from the economy this time. As long as the economy continues to strengthen, the story for the markets may be rotation toward the ex-Mag7 stocks.

As exhibited by our economic cycle model (see here), the US economy has been struggling with conditions that resemble a typical recession since early 2022 and has only recently begun to pull out of its malaise. One of the leading factors for the revival has been the ISM manufacturing PMI, which like our broad-economy indicator had been in contraction for most of that stretch only to pull into expansion starting this year. Likewise, the Federal Reserve Bank of Atlanta’s GDPNow – a real time forecast of GDP growth – is sitting at 3.3% for 2Q, hinting at economic acceleration ahead.

That pick-up in economic growth appears to be filtering down to earnings and may make for a different investment backdrop than has existed for years. From 2018-19, tighter monetary policy and the first round of Trump’s tariffs caused a broad based earnings decline. However, the magnificent-7 was able to pull out of recession faster and weathered the ensuing economic recession that followed in 2020 much better than the rest of the index, leading to dramatic outperformance that lasted until earnings for the 493 began to catch up. Likewise, in the initial part of the 2022 downturn, stocks lost leadership from the Magnificent-7 and decent earnings results for the rest of the index weren’t enough to keep the index afloat. Then as earnings for the 493 fell into recession in early 2023, mag-7 earnings began to pull out of their slumber, resulting in extremely narrow leadership that has helped drive the concentration risk concerns many express today. However, 2026 looks set up to be quite a different story, one in which the various segments of the economy begin to sync back up and move higher together. While the 493 are expected to lag Mag-7 earnings growth in 2Q, the group is expected to pull ahead of the mega-cap cohort in 3Q and maintain that lead into early 2027. Thus, whether the Mag-7 continues to cede leadership may come down to 2Q earnings reports and subsequent changes to analyst forecasts rather than a dramatic collapse in the index’s mega-caps.

Disclosure: HB Wealth is an SECregistered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.