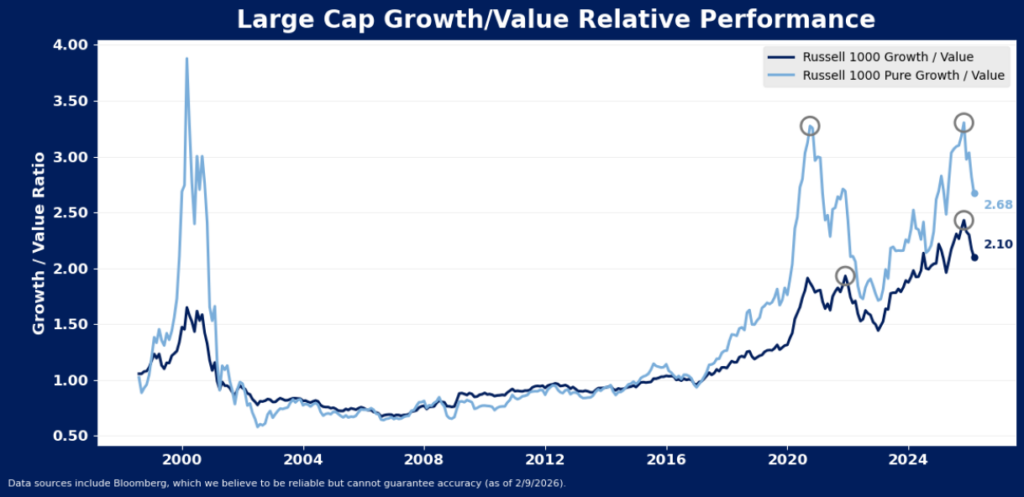

After outperforming for most of the last three years, growth stocks have been struggling relative to value stocks since October of last year. However, the broad indices may be masking a longer-term shift in the styles’ performance. Pure style indices and a look beyond large caps both suggest the growth style may be further past its relative peak than is commonly believed.

The Russell 1000 growth index hit a new high in October of last year relative to the Russell 1000 value index, leading to the conclusion that growth stocks at large were still making new highs in comparison to value. However, a look under the hood of the popular style indices reveals a different take – that growth outperformance was not enough to recover the style’s losses to value in 2021-2022. Growth stocks may have merely managed by their late 2025 peak to fall just short of their 2020 high relative to value.

Russell’s pure value and pure growth indices offer a finer take on style performance, as they have no overlapping constituents with one another. (On average, 25-30% of the constituents in the Russell 1000 growth index are also included in the value index. Thus, the pure indices can give an arguably clearer read on styles.) These indices show growth’s peak relative to value was all the way back in 2020 – the October 2025 peak in the Russell 1000 pure growth index relative to its value counterpart was slightly lower than the 2020 peak.

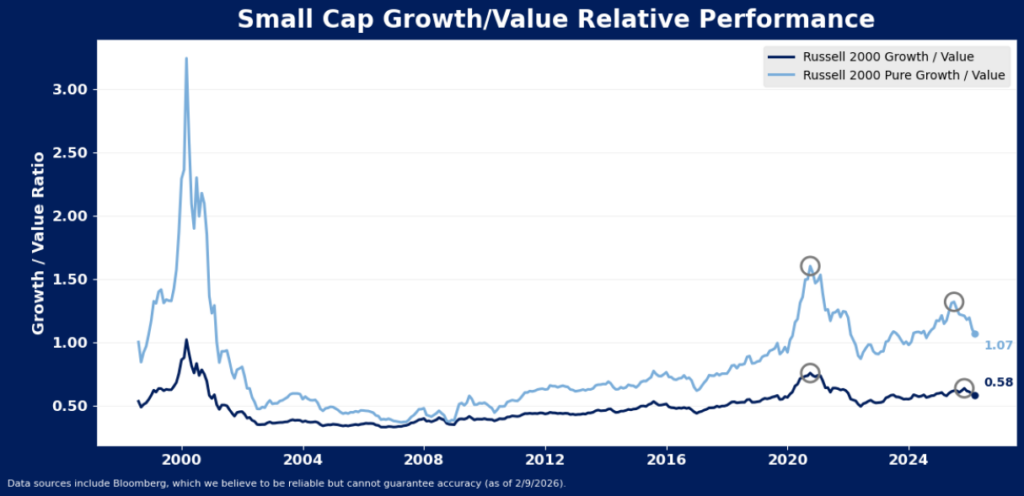

The small cap indices show a similar signal, though it is even clearer. In small caps, both the broad and the pure indexes show small cap growth peaked relative to small cap value in 2020, with the 2023-2025 rally resulting in a lower high for growth by comparison.

Disclosure: HB Wealth is an SEC registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.