Abstract:

- Russell’s reconstitution – when the provider assesses eligibility for the Russell 3000 and draws the breakpoint between the Russell 1000 and 2000 – is set for after the close on June 26th. This will be the first year since 1989 where Russell goes through this process semiannually, with the next change set for December.

- SpaceX will get all the headlines, set to join the Russell 1000 as a communications company under new fast-track rules, but SpaceX’s influence on the large cap float-adjusted index will be minimal. The bigger story is the graduation of several leading stocks from the Russell 2000 to the Russell 1000.

- Momentum typically slows down after reconstitution, leading to weak summer seasonality for small caps. Tech and industrials will lose significant weighting and many of the stocks that drove year-to-date leadership in the Russell 2000.

- This event does not change the long-term view but might add near term volatility. Relative valuations, improving economic conditions, and strengthening fundamentals remain at small caps’ back unless the Fed derails trends.

Russell’s now semiannual reconstitution will take effect on June 29th and the event looks poised to contribute some volatility to the index this summer as changes take hold. SpaceX will grab all the headlines, officially entering the Russell 1000 after Friday’s close but the real story may be how index changes impact small caps, and specifically if the Russell 2000 can continue its torrid year-to-date run after losing some of its biggest winners. Historically, both momentum factor and index gains slowed in the immediate wake of past reconstitutions as some of the strongest performers jumped into the Russell 1000. Additionally, the index provider plans to change to a semiannual reconstitution schedule from its once a year cadence this year, so benchmarks will face a second round of change come December. This could invite further volatility and erode seasonal tailwinds around year end.

Will Momentum Minus Small Cap Winners Keep Rallying?

Russell is set to do its reconstitution – when they reassess what stocks should be included in their indices and draw the breakpoints between large, mid, small and micro-cap gauges – after the close on June 26th. Using their provided list of additions and deletions from the existing Russell 3000 and “rank day” market caps – the day Russell locks company size to make its determination (April 30th this year) – we determine that 43 stocks are likely to graduate from the Russell 2000 to the 1000. Of those, 31 fall into the Russell 2000’s high momentum basket. This may blunt factor and index returns this summer as some of the best performing stocks become large caps.

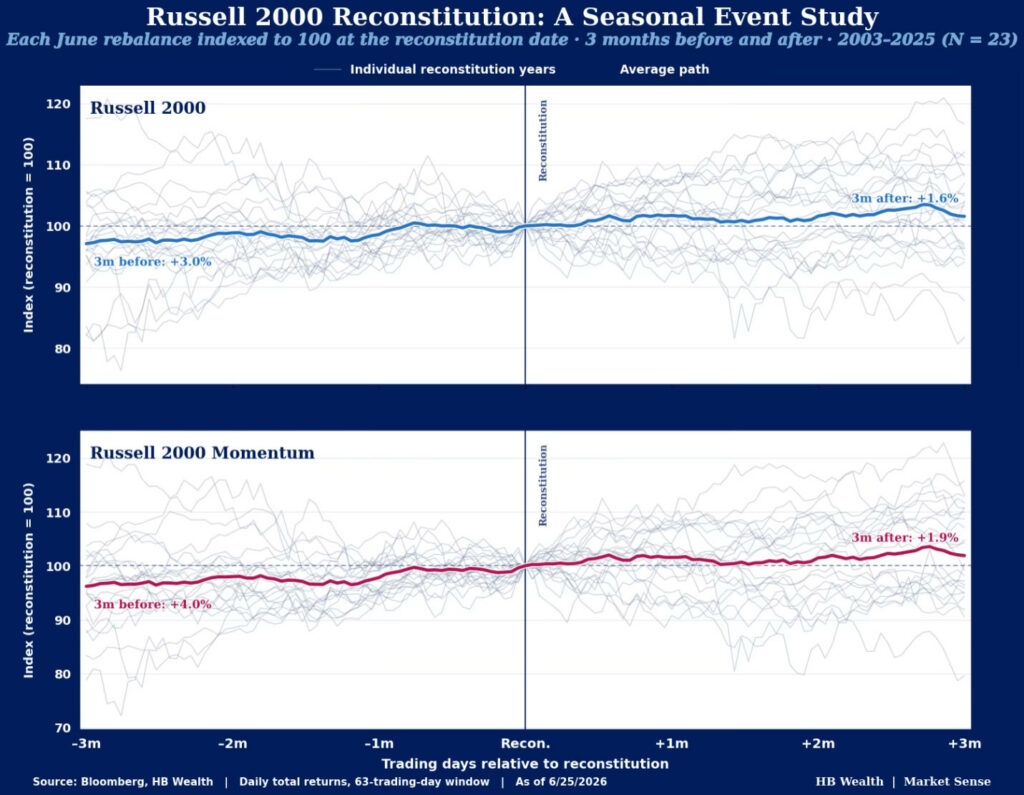

Russell index reconstitutions have a history of coinciding with a slowdown in both momentum factor performance and small cap relative performance trends. Looking back over 23 years of history in the factor, it is evident that momentum typically slows dramatically during the summer months that follow June’s reconstitution. On average, the long-only leg of Bloomberg’s PORT momentum factor rose 4.7% in the three months leading up to each year’s June reconstitution but gained just 1.9% in the subsequent quarter. Across the 23 observations, momentum posted worse returns 60.0% of the time after the event. Likewise, the Russell 2000 averaged a 3% gain going into reconstitution and was flat in the three months after with index performance worsening nearly 60% of the time post-June back to 1989 (when annual reconstitution was adopted).

This reconstitution may take the wind out of the sails of the small cap trade on a short-term basis as some of the best performers graduate to become large caps. On a sector neutralized long-only basis, momentum has been one of the best performing small cap factors year-to-date, up 22.9% and trailing only high beta so far in 2026. However, based on additions and deletions to the Russell 3000 set for this Friday, 31 of the 43 stocks likely to graduate from the small cap to the large cap gauge are roughly 8% of the 385 stocks currently in the top quintile of the momentum factor. On average, those 31 stocks have gained 95.5% so far this year, including Applied Optoelectronics and Bloom Energy – the 5th and 8th best performing stocks in the momentum basket so far this year are likely to graduate out. The former is up 310% year-to-date, contributing 0.26 percentage points to the index’s return while the latter is up 281% (contributing 1.8 percentage points).

Summer Seasonality Doesn’t Help, New Year Rally Could Lose Some Shine

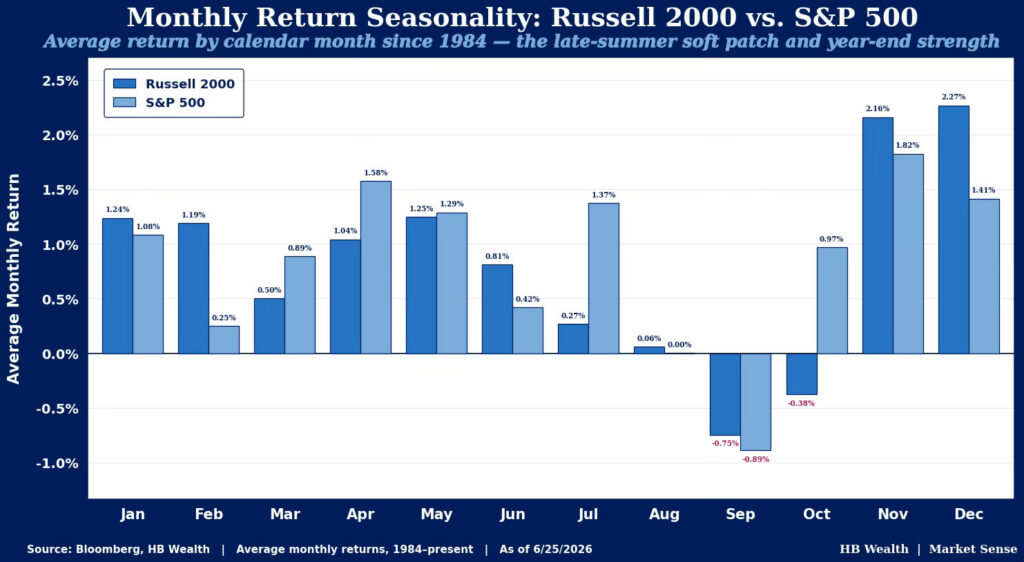

Seasonality is likewise a cross current working against the June rebalance schedule though part of the index’s summer swoon is at least caused by the event itself. Typically, summers are marked by lower volume and weaker gains in the Russell 2000. Since 1984, small caps rose an average 0.3%, 0.1% and fell 0.7% in July, August and September, respectively. That stretch encompasses three of the four weakest months for the gauge (October’s down 0.4% is the second-worst) and just so happens to coincide with the immediate aftermath of June’s reconstitution. While it’s easy to write off post-reconstitution weakness as summer seasonality, the same trends don’t exactly persist in the S&P 500. The large cap gauge instead typically surges in July (tied for its 3rd strongest month of the year, on average), with seasonal weakness emerging later in August and September.

Russell plans to add a second rebalance of its indices in December this year and in the future. At the index’s launch in 1984, it was reconstituted quarterly until 1987 when they switched to a semi-annual frequency. Since 1989, Russell has reconstituted annually with the index provider noting that in recent years, volume and volatility around the June reconstitution was high and there was significant style drift compared to peers that rebalance more frequently. However, adding a reconstitution in December might erode some of the new year rally that small caps typically enjoy. While December (up 2.3%) is the strongest month on average for the Russell 2000, January and February (up 1.2% each) are tied with May for third-strongest. That dynamic is similar to the S&P 500, where December is the second strongest month and its usually followed by a solid January. If the December reconstitution has the same effect as the typical June ones have had, it’s not unreasonable to think that some of the seasonal trend favoring small caps could fade each new year.

Industrials, Tech and Communications Sectors Shaken Up Most

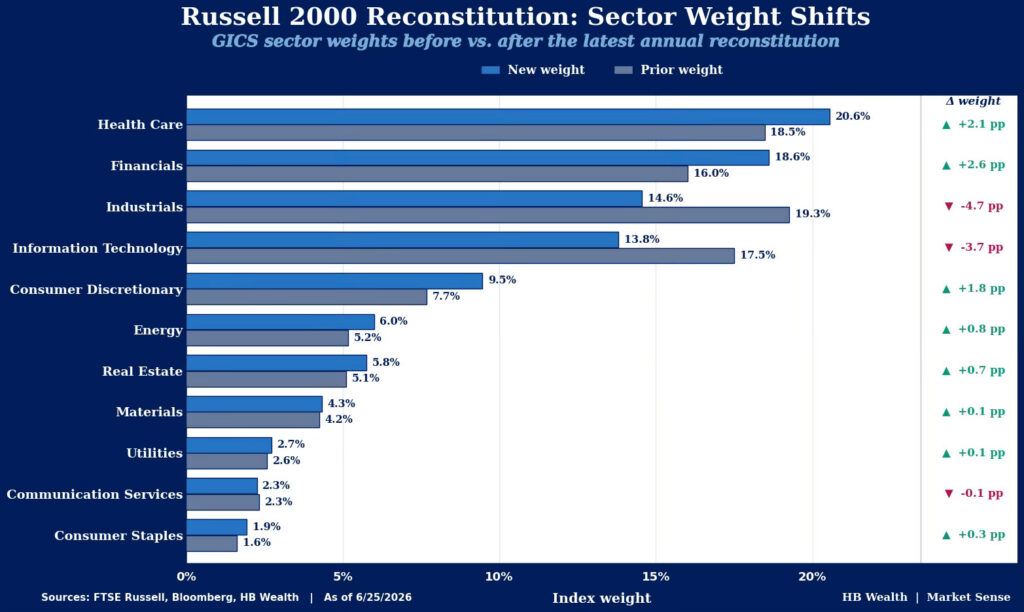

The biggest (and most controversial) change this reconstitution will be the addition of SpaceX to the Russell 1000 via new “fast track” rules. Like other major US indices – except the Dow which is price-weighted – Russell uses float shares to calculate index weights which will keep its influence down for now. Based on Bloomberg data, SpaceX carries a $97 billion float-cap which would put it at the 115th largest stock in the gauge and lift communications’ weight by about 5 bps. Due to the large size of Russell 1000 constituents, sector concentrations shouldn’t move too much – we anticipate a maximum 32-bps weight gain in industrials. Conversely, Russell 2000 weights could shift more, with tech (minus 370 bps) and industrials (minus 470 bps) losing the largest share thanks to large graduates driving a sizable reweighting toward financials and health care – making them the largest groups in the index from second and fourth pre-reconstitution.

Given how this year has gone it should be no surprise that industrials and tech dominate the 42 stocks set to graduate to the Russell 1000. Year-to-date, tech (up 44.7%) and industrials (up 29.5%) are the best performing sectors in the Russell 2000. However, industrials could lose the largest number of stocks (16) to the Russell 1000, followed by tech (15). Additionally, the stocks leaving industrials and tech had contributed 19.8 and 24 percentage points, respectively, to the sectors’ year-to-date gains. Those strong performers are unlikely to be replaced and of the 36 companies we identify as possibly being demoted to the Russell 2000 from the 1000, only 3 and 5 companies are in industrials and tech, respectively – likely shifting some of the sector concentrations within the small cap gauge.

Longer Term View Remains Intact but Watch the Fed

While rebalance may slow small caps’ torrid run as summer doldrums set in, the longer-term favorable outlook for the group remains unchanged – low relative valuations, improving macroeconomic conditions, and strengthening fundamentals remain strong tailwinds for the Russell 2000. The biggest risk to small caps is not likely the reconstitution of the index, but the Fed. Kevin Warsh’s first press conference indicated a strong desire from the Fed to maintain price stability, and rate hikes can often be troubling for small caps that have higher costs of capital than larger peers. Thus, a policy mis-step that harms the economy is the real threat to smaller companies. If the Warsh Fed does begin hiking this year, the central bank will need to thread the needle by stifling inflation but leaving other macroeconomic tailwinds intact to keep small caps running ahead of large cap peers.

Disclosure: HB Wealth is an SECregistered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.