Market Sense

By:

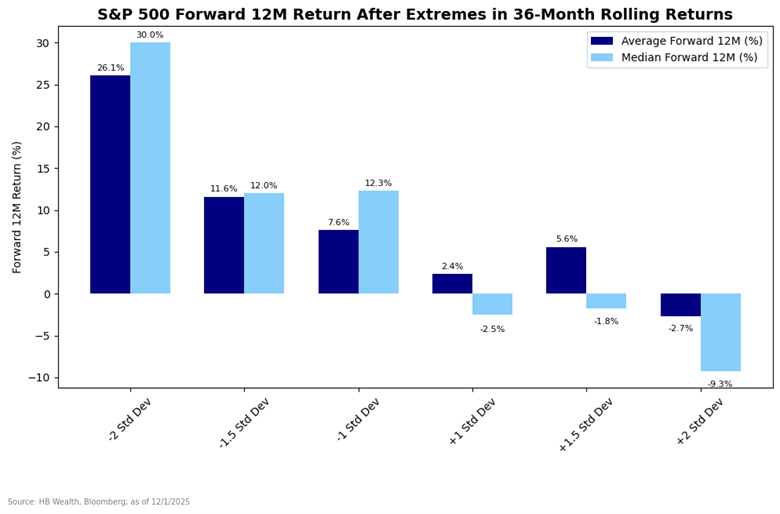

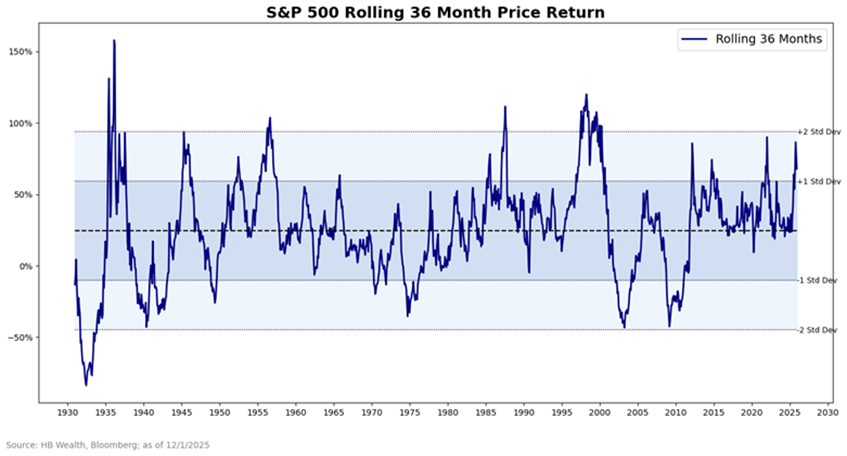

The S&P 500’s 36-Month Rolling Return neared 2 standard deviations from norm in September. The chart below shows what historically happened after extremes were reached in the measure. The more extreme the deviation, the lower the return prospects. Likewise, such extreme deviations above norm generally lower the probability of a…

The annual prognostications for equity market returns are rolling out as the end of the year approaches, and the current strategist consensus suggests a moderate 5% return is likely. Historical patterns support these low expectations, for the S&P 500 has crossed a critical threshold that implies a strong likelihood of…

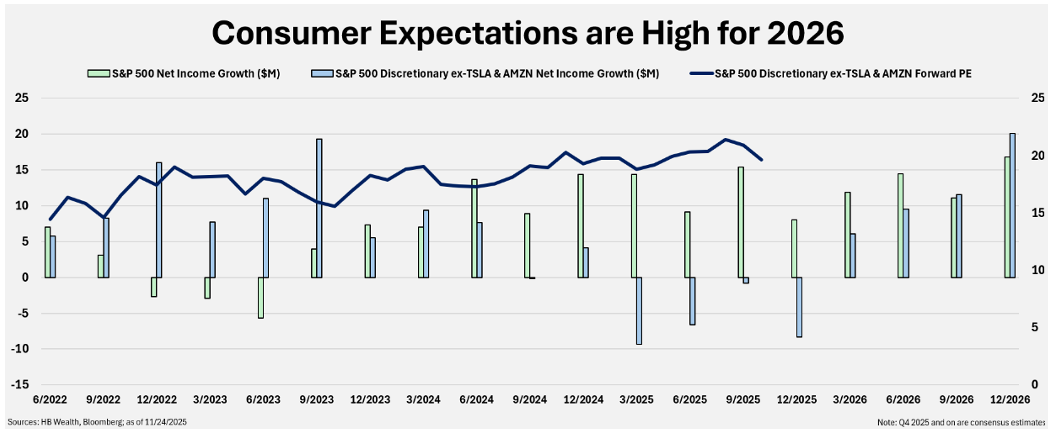

Thanksgiving week normally kicks off a period of positive seasonality in stocks, in part because the U.S. consumer rarely disappoints during the holiday season. But high market expectations for recovery in 2026 may be tough for the consumer to overcome in the year ahead. Consensus and market implied expectations for…

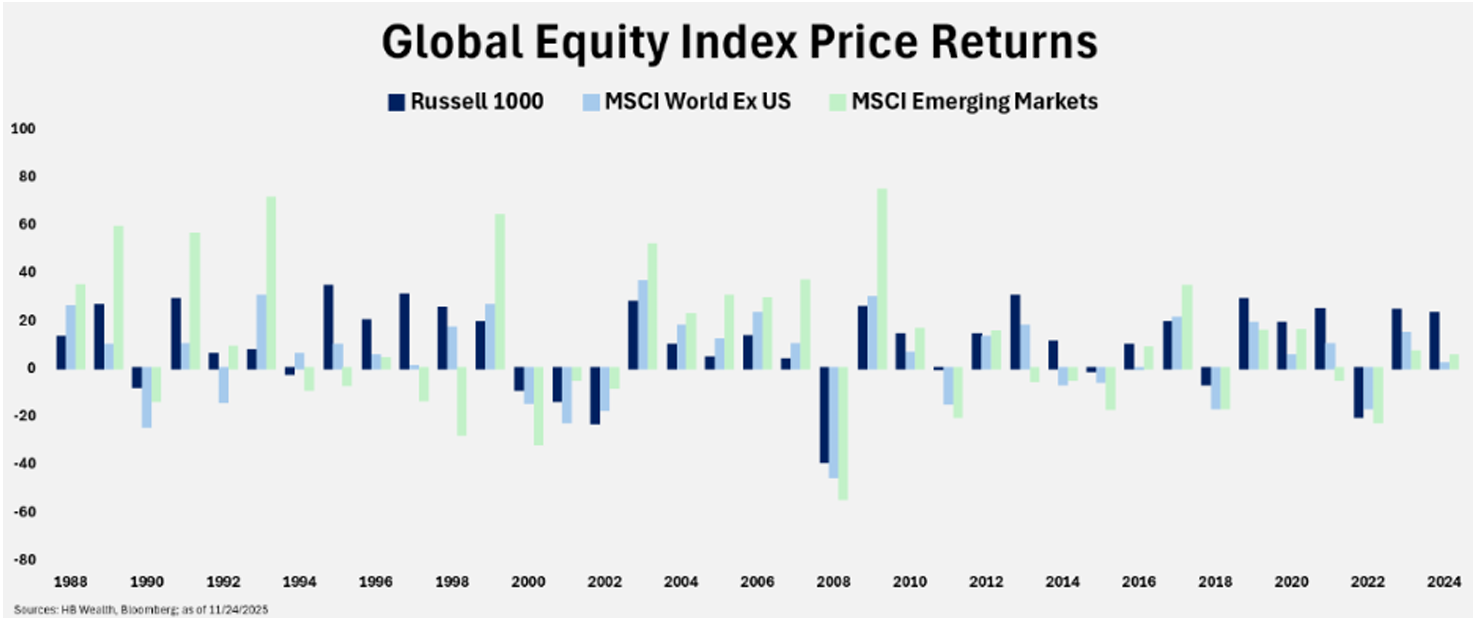

International stocks are on their way to their first year of outperforming domestic stocks since 2017, and strengthening earnings, discounted valuations, and dollar depreciation may all continue to make the case for global shares to perform well into 2026. U.S. stocks (represented by the Russell 1000) are up 13% so…

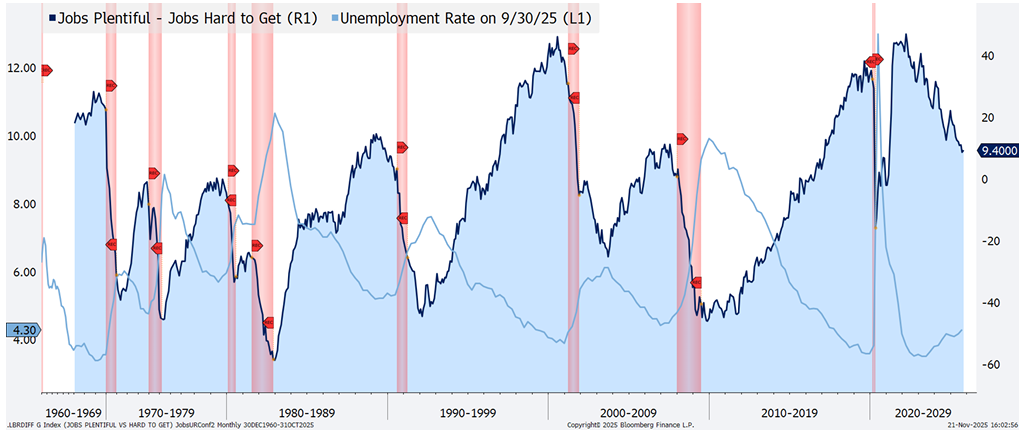

The jobs market has signaled a weak economy for years, even as other indicators such as corporate profits suggest the economy is holding up reasonably well. This may help explain why consumer confidence remains near record low levels, even as the stock market is at record highs. The unemployment rate…

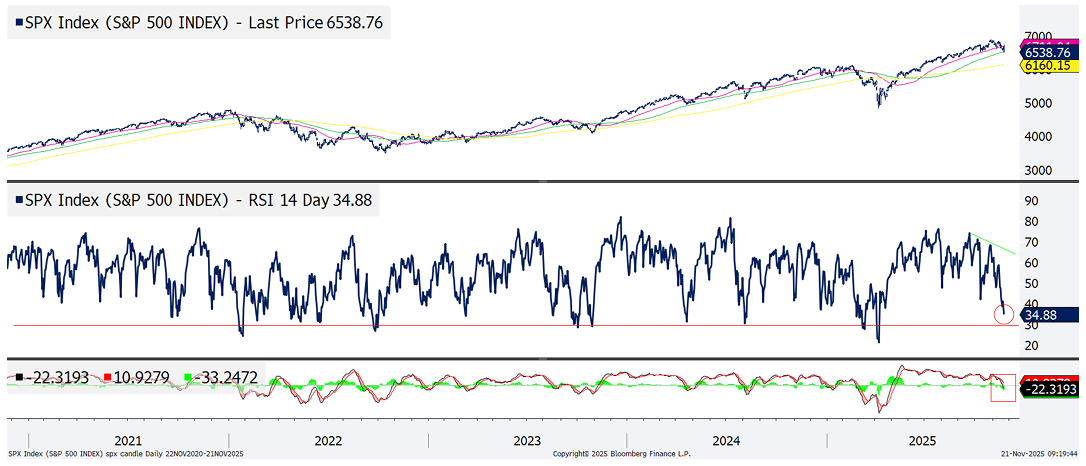

The longer-term equity bull market remains intact, supported by S&P 500 moving averages that are still trending higher, but stocks’ short term sell-off looks likely to deepen nonetheless. Momentum, represented by 14-day RSI, is not yet oversold and MACD (moving average convergence divergence) has just crossed into negative territory, hinting…

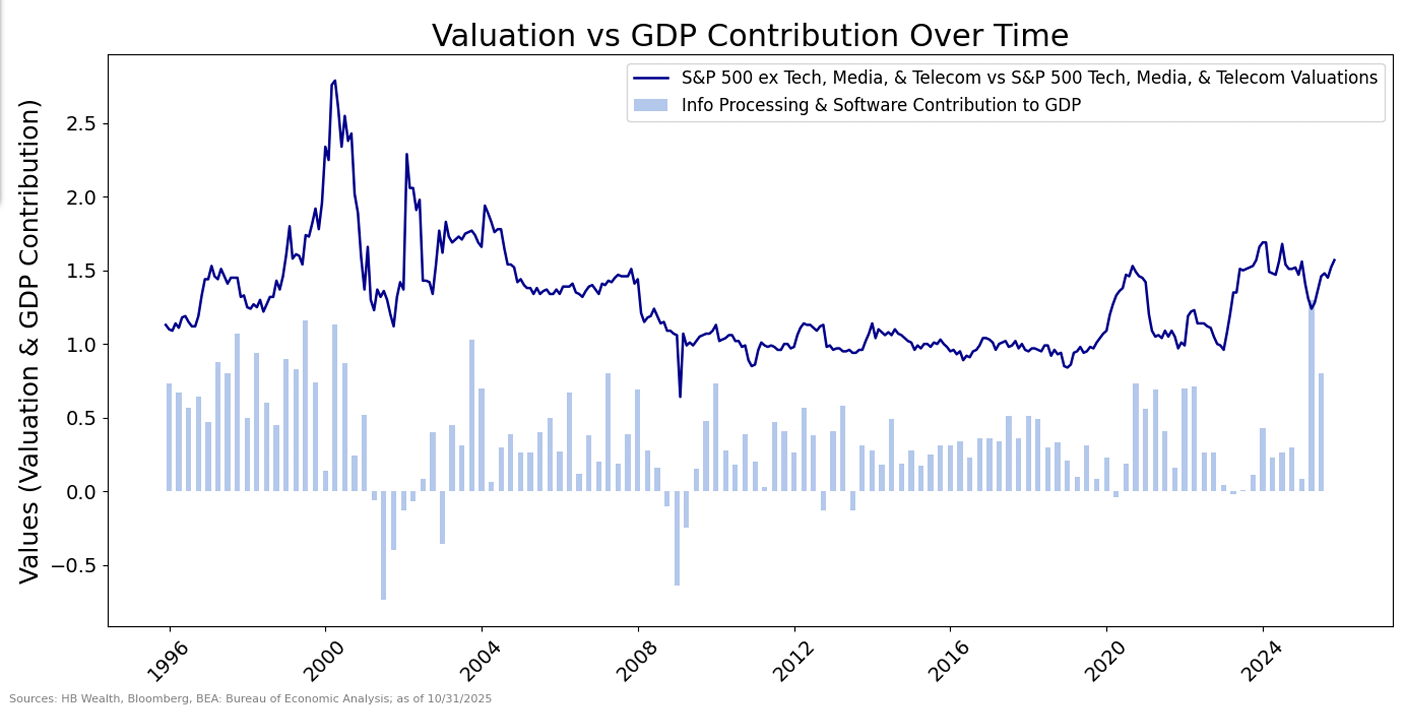

The equity market is enthusiastic about prospects for AI spending to remain a primary driver of earnings growth, and while a cooldown in valuations may be needed to keep expectations from getting too far detached from reality, both investment trends and stock multiples are less extreme than they were in…

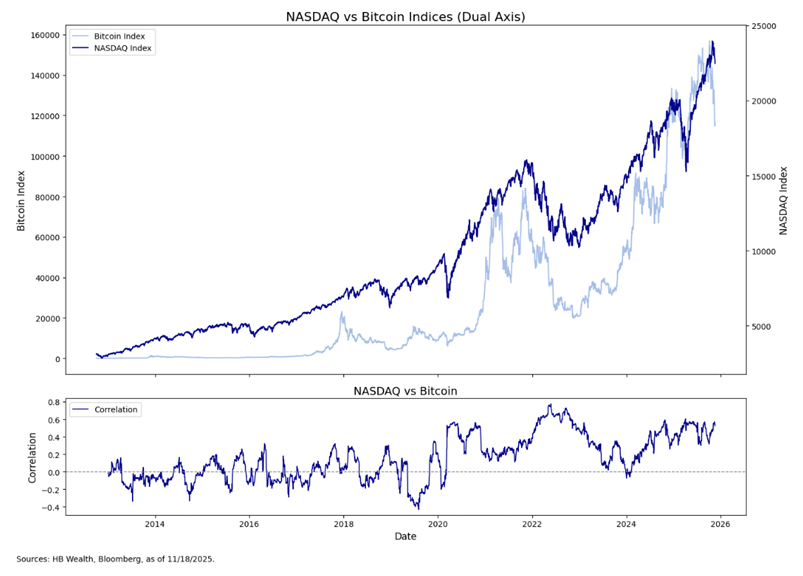

Bitcoin is down more than 25% from its peak in early-October, and this doesn’t bode well for U.S. tech stocks, which have dropped less than 6%. If past proves precedent, and unless Nvidia can revive confidence with their earnings report tomorrow, US tech could be due for a bigger decline…

- « Previous

- 1

- …

- 3

- 4

- 5