U.S. large cap stocks have broken down through the key 100-day moving average support level as the simultaneous gain in oil prices and deterioration in employment added to the AI-fears and private credit strains that have been nagging markets for months. It is extremely rare to see job losses and oil price surges of the current magnitude simultaneously. If war in the Middle East persists amid weak hiring, equities will likely continue to struggle, and the market will need to price rising economic recession risk.

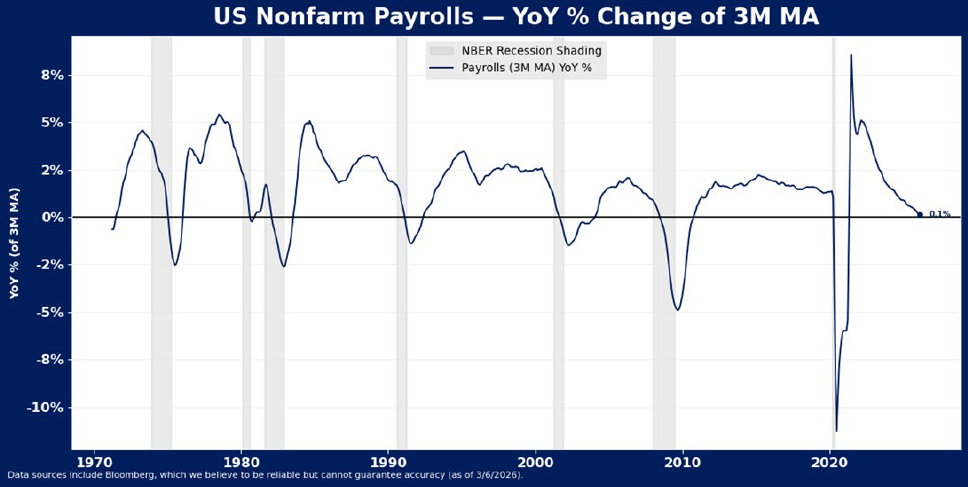

Fragile Jobs Market Weighs on Outlook

The economy shed more than 90,000 jobs (0.06% of total jobs) last month, something that usually only happens when the U.S. is in the throws of an economic recession or trying to climb out of one. In history going all the way back to the 1930s and excluding recessions and the year just after recessions (job gains are volatile in the early stages of economic recovery), we found only 25 other single months (2.4% of total months) in which jobs dropped by at least 90K. This is less than 3% of the time.

February weakness may be due to a combination of temporary disruptions like a labor strike and winter storms, and weakness may be exaggerated by adjustments to the Bureau of Labor Statistics’ updated “birth-and-death” model of business formations. Yet, the 3-month moving average job gain was also just 5.7k. That’s down 71.3k from the same time last year as suggests a troubling trend in jobs has emerged. There is no historical precedent for job growth this weak outside of recession experiences.

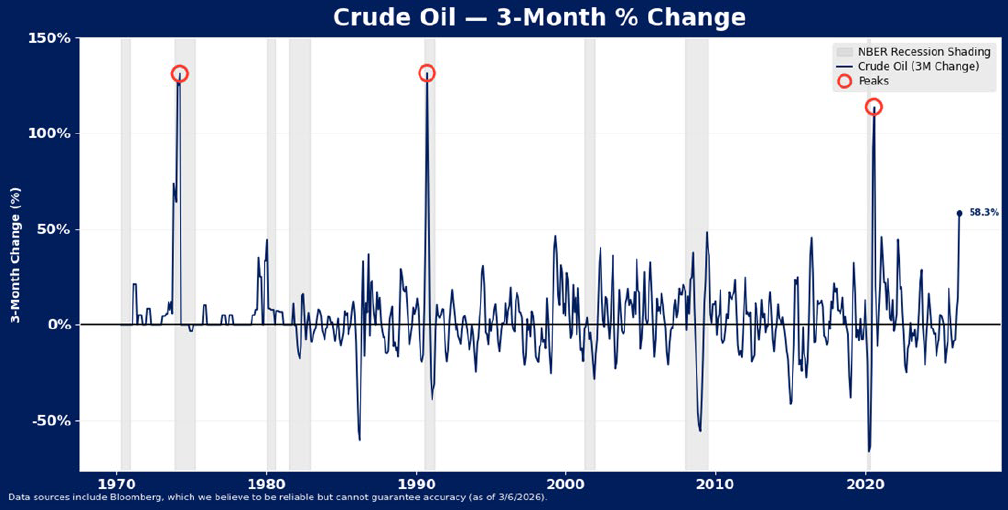

Oil Shock Amid War in Middle East

As if that weren’t enough for the market to absorb, the jump in oil prices last week broke records. Brent crude oil rose 27.3% and West Texas Intermediate rose 35.3% in a single week. The magnitude of the weekly oil price gain is extremely rare. There have only been 5 other times prices jumped that much in a week in the last 35 years – all of them were during and just after the 1990 and 2020 recessions.

The price of oil is on pace for its fourth largest gain in history on a rolling 3-month basis. If the oil price gain sticks through March, it will be one of the biggest monthly oil price spikes in history. There were only 6 other months since 1970 in which oil prices jumped as much as they did last week. Notably, the economy generally struggled with these price spikes – 4 of the oil price gains occurred during or within a year of recession experiences.

Signal from Jobs +Oil is Troubling

Simultaneous job loss and oil price spikes are trouble for the economy. They have occurred very rarely and usually only around recessions. The only months in the last 35 years in which the economy sustained a job loss as large as February and oil price jump as big as that recorded so far in March (both in percentage terms), were during the Gulf War in 1990, and the recession recoveries of 2002, and 2009.

History of the economy’s ability to withstand combined oil price and job shocks that last more than three months is particularly grim. Indeed, the only time in history in which oil prices were above $90 and job losses were stacking up was the Great Financial Crisis. Each time oil prices rose more than 30% and jobs fell for three months the US fell into recession, with only one exception, and that was at the tail end of the tech bubble in 2003.

Conclusion

While the spike in oil prices may prove short lived if war in the Middle East, the rapid escalation in oil combined with the job market signal is currently not favorable for risk assets. Should the spike in oil and weakness in jobs cues continue for another few months, it will increase recession risk materially for this year. This is highly contrary to consensus expectations for economic acceleration and double-digit earnings growth, and may force continued re-pricing of risk across financial markets. As long as job weakness and high oil prices persist, they will suggest defensive strategies are likely to perform best.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.