Though the headline decline in the S&P 500 of 3% over the last two weeks may at first appear benign, underlying supports for the index are fading fast, as war in the Middle East has depleted breadth at the stock and sector levels. While most investors are watching the price of oil for signals, the stock market is also likely to get its cue from financials, the second largest sector by market cap in the S&P 500, and an early cycle indicator for the economy. Even if war is resolved and the price of oil calms, financials participation will be key to a durable market advance.

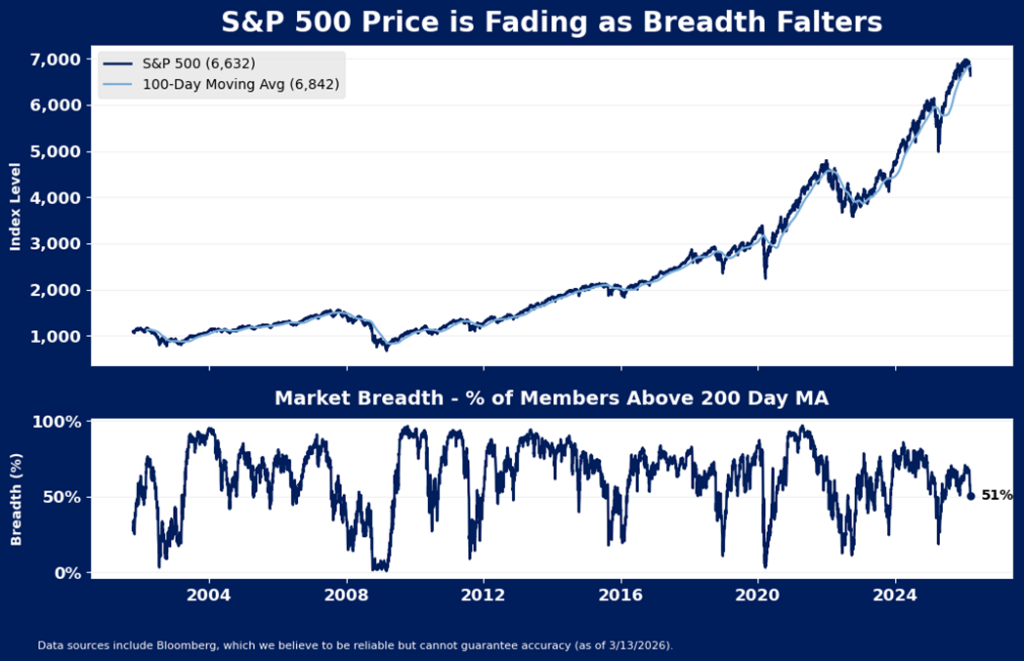

S&P 500 Breadth is Deteriorating

The S&P 500 is losing its breadth at both the stock and sector level, suggesting that the 3% drop in the index year to date may be masking emerging weakness. The percentage of stocks on the index that remain above their 200-day moving average has dropped near fifty, a level that usually offers support during uptrends. While short-term losses of breadth can occur with no consequence on occasion, a longer-term breakdown in breadth below the 50% level could indicate more severe stress is emerging for the index. Notably, each correction of 10% or more in stocks over the last twenty years has occurred with this confirming breadth cue.

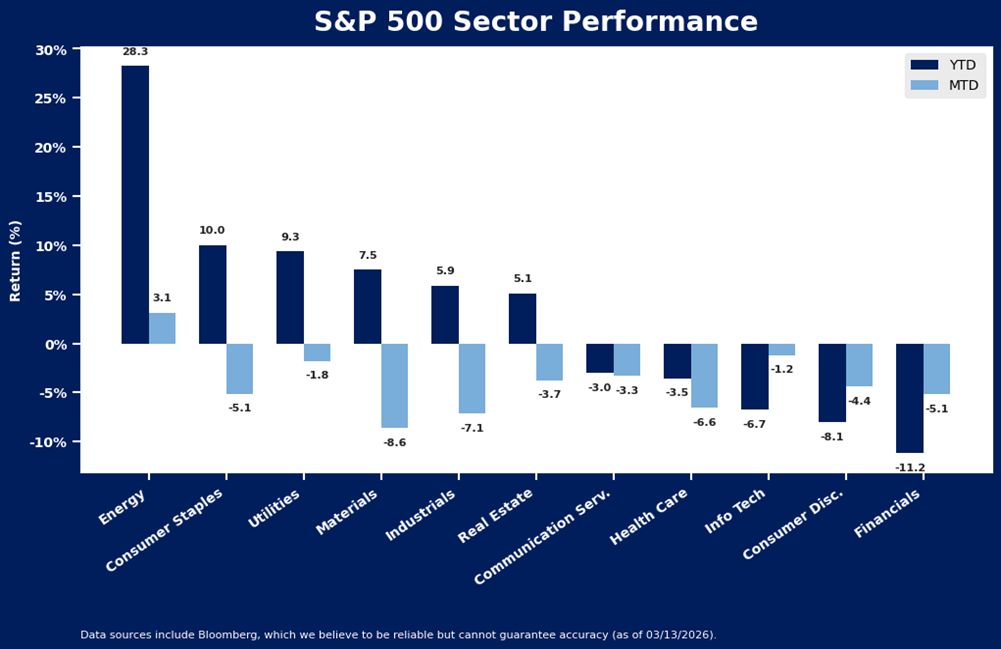

Energy is now the only sector in the large cap index with positive short- and long-term momentum. Though the energy sector has had a stellar year, up nearly 28%, it is highly unlikely that this group can manage to hold up the market alone. At less than 4% of market cap of the index, energy is too small to keep the index afloat on its own, and its identity as a cost input to the other sectors creates broader complications for earnings. Prior to the breakout of war, staples, materials, industrials, utilities and real estate were all also posting gains this year, but all of those sectors have sold off since the war began, leaving little upward momentum remaining in the S&P 500.

Financials Cue Should be Watched Most Closely

While the markets remain captive to the price of oil in the short run, financials stocks may be the more meaningful indicator to watch for longer term market direction. Financials are the worst performer among sectors in the S&P 500 so far this year. The group is down more than 11%, more than 4X the decline in the market at large. That’s the worst 10-week performance for the sector since April 2025.

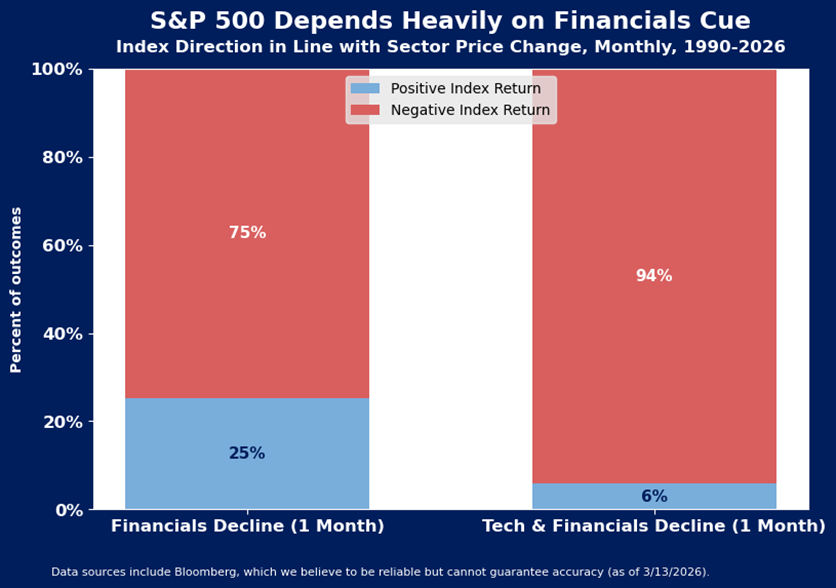

Financials entered the year with lofty expectations, indicated by valuations at levels last recorded prior to the Great Financial Crisis, which may have made the sector more vulnerable to disappointment. Nonetheless, the tough combination of private credit strains, the flattening yield curve, and threats of policy intervention in the housing and banking industries may continue to suppress returns for the group. This may remain a problem for stocks at large. Since 1990, a monthly loss in financials coincided with a monthly loss in the broad market 74.7% of the time, with financials down in 182 months and the market down 136 of those months. When financials and tech are struggling together, as has been the case for most of 2026, It is even more unlikely the market at large can rise. When financials and tech sectors both sold off, the market dropped in 94.2% of months.

While the price of oil and performance of energy stocks may continue to draw the lion’s share of attention in the near term, we think financials may offer a stronger indication of the longer-term trend. Financials loss of momentum prior to the war and continued struggles during the last two weeks is notable, and hints that even without the war, a meaningful disruption in the market and economy may be underway.

Disclosure: HB Wealth is an SEC‑registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.