")

International equities meaningfully outperformed US stocks last year, but the value of holding non-domestic stocks extends well beyond returns. Critically, correlations among markets have been falling and dispersion of returns between regions has been rising as well, elevating the diversification benefit of international stocks. As geopolitical and trade risks continue to evolve and widen the gulf between global economies, non-domestic equities may remain a source of portfolio ballast.

Equities are Less Correlated as the World Economy Decouples

The case for global equity ownership extends well beyond relative returns. As world trade volumes have declined and the world decoupled, global shares have offered significant and potentially still underappreciated diversification benefits to equity portfolios.

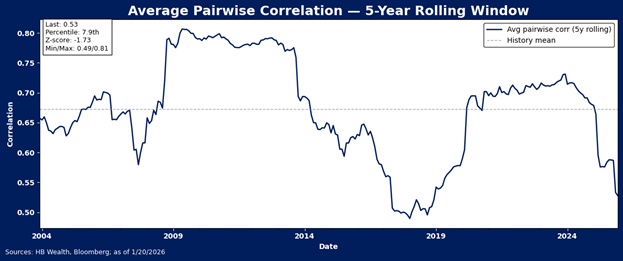

Relative to five-year norms, correlations among major country markets largely dropped over the last year, extending a trend of falling correlations in global equity markets that began again in 2024. Five‑year rolling average correlations across global equity markets have fallen to their lowest level since 2019. Our analysis of rolling five-year correlations across shows the current reading is sitting roughly 1.73 standard deviations below the long‑term average observed since 2004.

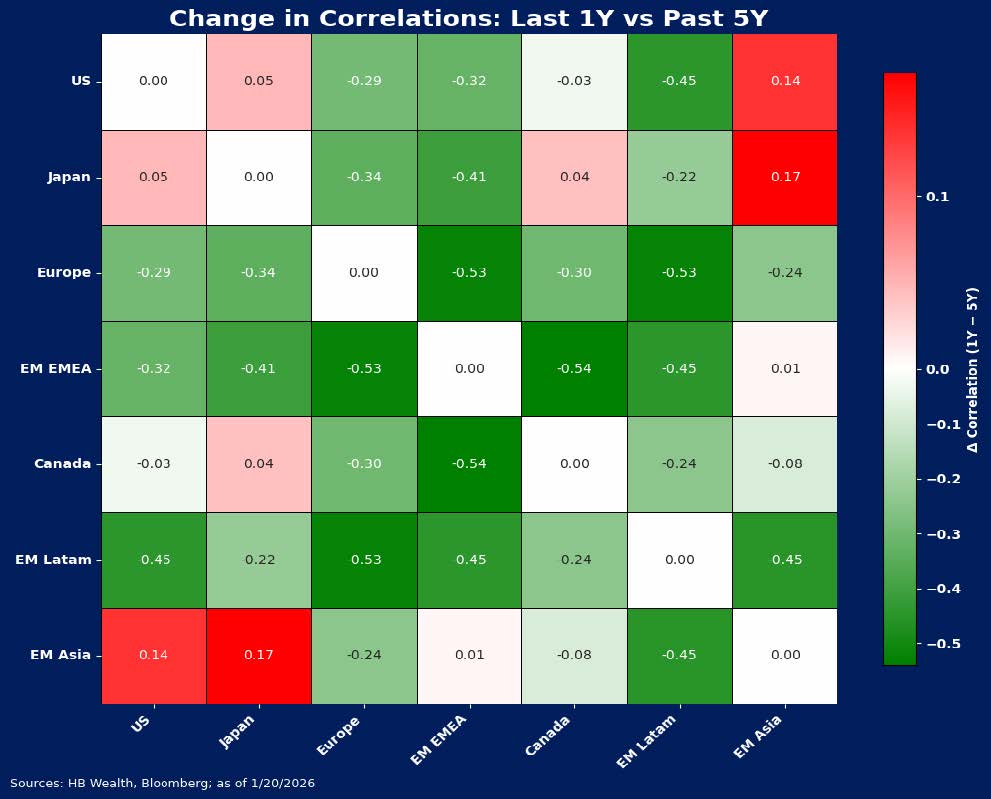

Over the last year, Europe, emerging markets, and Latin American equities all became less correlated to the U.S. equity market, and emerging markets at large decoupled from developed markets. Europe and Latin America showed particularly broad declines in correlation with other global equity markets. Among major markets, the only significant increases in cross-market correlations emerged between the US, Japan and EM Asia, as technology sector concentration tied these markets more closely together.

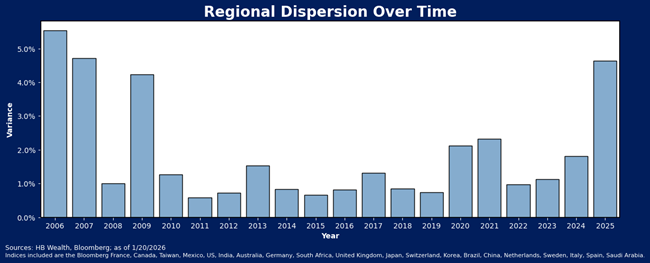

Notably, declining correlations are not the only wind at the back of international equities. Material diversification benefits can also be achieved as dispersion (or variance) rises, and dispersion of returns across the top global markets also rose to its highest level in nearly 20 years in 2025. On average, return dispersion was extremely low in the decade after the financial crisis, but has been generally higher in the years since the pandemic, as regional growth divergences and thematic influences have taken on a stronger role in driving returns amid geopolitical strains. Notably, dispersion hit a level last year that is closer to the pre-crisis norms, when US stocks were less consistent leaders of world equity returns.

Disclosure: The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.