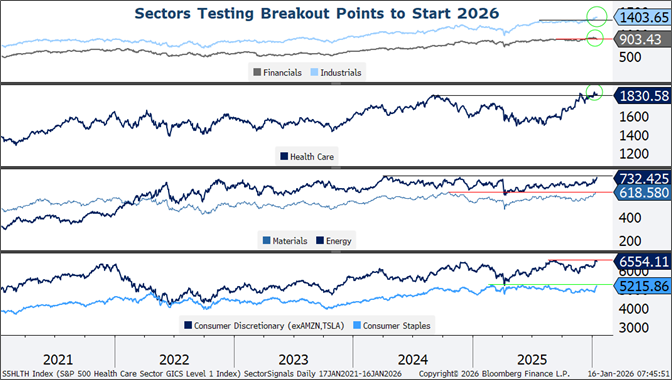

Domestic growth themes based on policy support and regulatory reprieve have largely driven equity market rotation out of tech and toward other sectors in the US equity market in recent months. Renewed geopolitical turmoil and some disappointment on the domestic policy front now threatens to upend the party in 2026. All sectors but tech and financials are up to start the year, but only industrials – the sector that threads the needle of both domestic recovery and geopolitical risk – has decisively broken out beyond former resistance levels. As policy headwinds continue to shift, we expect company commentary around how it may impact earnings trends in the next few weeks may help discern winners from losers in the U.S. equity market.

Commodities and Consumer May Battle

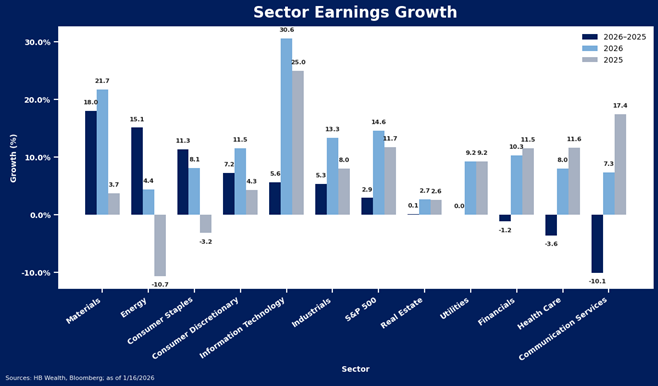

The strongest earnings turnaround in the S&P 500 is expected to come from a very unusual combination of both consumer sectors and commodity sectors in the year ahead. Consumer staples and consumer discretionary sectors are anticipated to both growth in 2026 after recording earnings declines in 2025, thanks to a presumed consumer recovery as well as margin gains with lower inflation pressures. Fed rate cuts and easing financial conditions are supposed to help get debt-financed consumer spending growing again while tax refunds help spur a recovery in disposable income growth, which has recently stagnated with wages and jobs. This should help topline, while reduced trade risks and moderating inflation contribute to margin growth for this group.

Meanwhile, energy and materials are expected to record an even stronger earnings recovery. Raw industrials, oil and precious metals prices are rising much faster than equity prices so far this year, as elevated geopolitical risks are helping spur a surprising break higher in commodities prices, adding to fundamental upside for the groups.

While energy and materials clearly benefit from higher prices, consumer spending and consumer sector margins are susceptible to downside shock as oil prices rise. Thus, while not impossible, the notion that both consumer sectors and commodity sectors will simultaneously lead recovery seems somewhat improbable, and dependent on how much geopolitical risk evolves in the weeks ahead. Outperformance of domestic cyclicals will only likely continue if commodity price gains are contained, and vice versa – commodity sectors will likely only lead if price appreciation remains.

Regulatory Risks May Make or Break Health Care and Financials

The most policy-sensitive segments – financials and health care – are on the other end of the earnings growth momentum scale, both anticipated to post growth in earnings, but at a slower pace than was recorded in 2026. Despite this inferior relative earnings position, both sectors have toyed with breakouts so far this year, perhaps due to anticipated policy and regulatory reforms. This will leave both sectors somewhat vulnerable to those very regulatory and policy headlines to keep their trends moving higher. Financials have been recently plagued by White House remarks about housing and credit card rates, and health care faces significant challenges stemming from expiration of Affordable Care Act financial assistance.

Industrials In-Between

The industrials sector does not have the strongest anticipated earnings momentum in the index, but it may benefit most among sectors from the combination of policy support) as well as rising geopolitical risk. Tax reform promotes capital spending to boost industrials’ revenue while lower short-term rates ease the sectors’ heavy debt burden. Meanwhile, geopolitical turmoil and rising global defense budgets directly support the defense industry. Higher commodity costs may elevate input prices for some but benefit topline growth for more.

In summary, the year has started off with all sectors but tech winning, but the themes that have driven gains so far are likely to be tested as the year progresses, leading to greater dispersion at the sector, industry and stock level in the S&P 500. If tech comfortably settles into the backseat, new drivers will emerge, but not likely all at once.

Disclosure: The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.