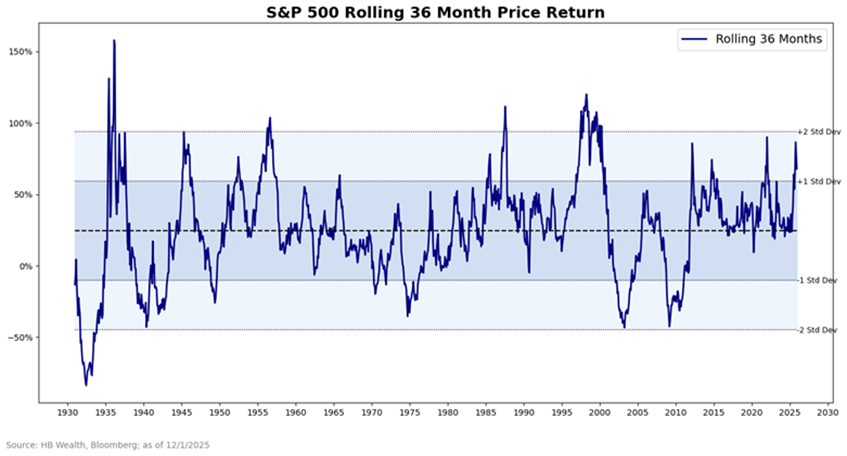

The annual prognostications for equity market returns are rolling out as the end of the year approaches, and the current strategist consensus suggests a moderate 5% return is likely. Historical patterns support these low expectations, for the S&P 500 has crossed a critical threshold that implies a strong likelihood of a slowdown in stock price growth in the year ahead.

The trailing 36-month price return reached nosebleed territory in 2025. For the first time since 2021, and only the 16th time since 1930, stocks trailing three-year return hit levels more than 1.5 standard deviations above average. Using post-WWII returns only, the 36-month rolling return nearly touched 2 standard deviations above average in September and has been easing off that high with the last two months of market churn.

Historically, slower returns tend to emerge after such extremes. On average and median, stocks have struggled after reaching at least a standard deviation above long-term average rolling 3-year returns. The more extreme the deviation, the lower the return prospects, according to history, with 2 standard deviation moves in stocks affiliated with an average forward decline of nearly 3% and median drop of 9%.

HB Wealth is an SEC Registered Investment Adviser and the information provided is for informational purposes only. Additionally, the information should not be construed as investment advice or a recommendation to buy or sell any security or other financial instrument. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. The views expressed are those of the author and do not necessarily reflect the opinions of HB Wealth. Please consult your financial advisor before making any investment decisions.