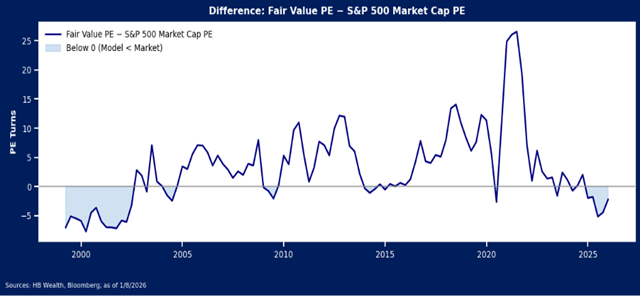

Our macro model for S&P 500 valuations shows multiples have jumped too far ahead of macroeconomic support and this may slow the pace of index price growth in the near term. This model suggested markets were largely undervaluing low interest rates for most of the last two decades, supporting the case for multiple expansion and robust price growth. Now it suggests that the market is overvalued. The last time our valuation model fell this far short of the market was during the tech bubble, but the model also shows stocks’ valuation excess is quite small by comparison to that time.

Valuations are notoriously poor timing tools and thus should be just one component of a decision process. Nonetheless, our model for valuations suggests a slower growth landscape for stocks may be set to emerge in the year ahead. Based on current consensus expectations for the 2-year and 10-year Treasury yields, as well as forecasts for earnings growth to rise about 14% per year for the next two years, our regression model for US large cap stocks suggests the S&P 500 should trade closer to 19X earnings versus its current P/E ratio of about 22x.

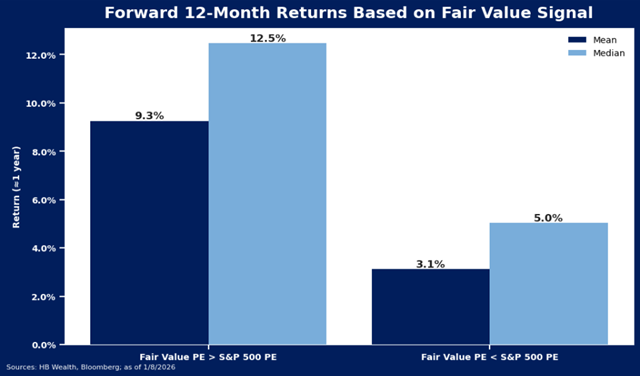

Since 1999, in periods when the market P/E was below our model estimate, forward 12-month returns for the market averaged 9.3%, and the median return was 12.5%. Over 40% of the market return in these periods came from valuation expansion. Now that the market has gotten ahead of the model estimate, it implies lower expected returns for stocks. Or, at least, returns that are more dependent on earnings growth than on valuation expansion. Over the last 26 years, when the market PE was above our modeled PE, the market return averaged 3.1% and valuation expansion accounted for slightly less (35%) of the return during those periods.

While 2025’s excess is still modest by comparison, the only other extended period when the combination of bond yields and earnings growth undershot market multiples was during and just after the turn of the century tech bubble. At that time, the model undershot market multiples for several consecutive years, and by a much larger margin. Our model suggested the market was overvalued from March 1999 to June 2002, or 39 months, and by up to 7.7 turns. At max this time, our model suggested the market was 5.2 turns overvalued, and the model has hinted at excess valuation for the last 15 months.

Prior to this past year, the market only became overvalued by comparison to its macro supports for brief stretches, and excess valuation was minimal. This mandated an optimistic outlook for valuation expansion to contribute to price appreciation. The model now suggests valuations are a risk to stocks. Thus, multiples may be more likely to compress to align with the rates landscape, effectively slowing down the pace of the bull charge in stocks in the year ahead.

Disclosure: The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.