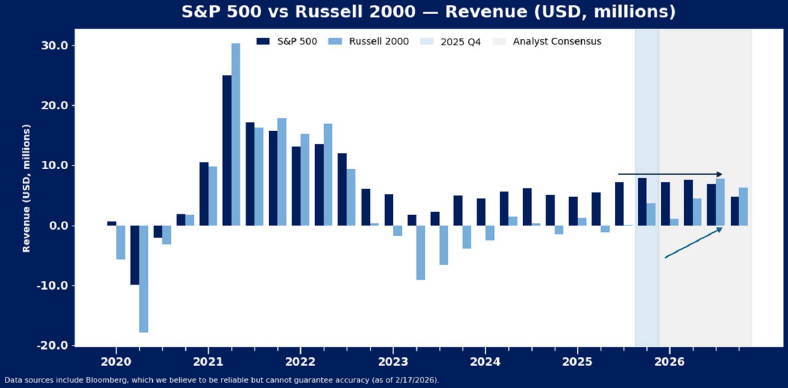

Earnings season is normally an uplifting experience for the S&P 500, but that has not been the case in recent weeks. On the surface, earnings appear fine, with the index on pace to post about 13% growth in earnings compared to the same period a year ago, and revenue rose almost 8%, the fastest pace since 2022. About 75% of companies posted better results than analysts forecast at the start of the season. However, evidence has emerged that the quarter just passed may be as good as it gets for the next year, at least for S&P 500 topline growth. Momentum in revenue has been a tailwind for stocks since early 2023, but if analysts are correct, revenue growth may have peaked in the fourth quarter of 2025 for the large cap index, and for cyclical stocks within the S&P 500. Meanwhile, small cap stocks are picking up steam as revenue recovery appears increasingly likely to emerge. This mix creates a mixed picture for the outlook, and results for now in a churning equity market at large, with small caps and defensive sectors simultaneously outperforming.

As Large Cap Momentum Peaks, Small Caps May be Revving Up

S&P 500 revenue growth may have hit peak pace in 4Q 2025, at 8.1% YoY, the fastest growth since 2022, and much faster than the average pace of growth of about 5% since 2023. Revenue growth above 8% on the index is historically somewhat rare outside of recession-recovery periods. In the pre-pandemic cycle, the S&P 500 posted growth of greater than 8% just one time, in the fourth quarter of 2018, the quarter that proved to be peak growth for the index. On average from 2014-2019, the index posted about 3% revenue growth.

Unlike large caps, which may be reaching a peak pace, small caps have a longer runway for improvement in revenue growth. The divergence between small cap and large cap revenue trends is a unique feature of the post-pandemic corporate experience. Small cap revenues have failed to reach lift-off since they went into recession in 2022, and while the large cap index was recovering over the last three years, small caps failed to post persistently positive growth. If the analyst community is correct, small caps may just be entering a more sustainable growth phase. Small cap earnings season is still underway, but the group is on pace to record 3.7% growth in 4Q, the first quarter of above 2% growth in three years. If consensus is correct, small cap revenue growth may stall temporarily in 1Q, but pick up momentum through the remainder of 2026.

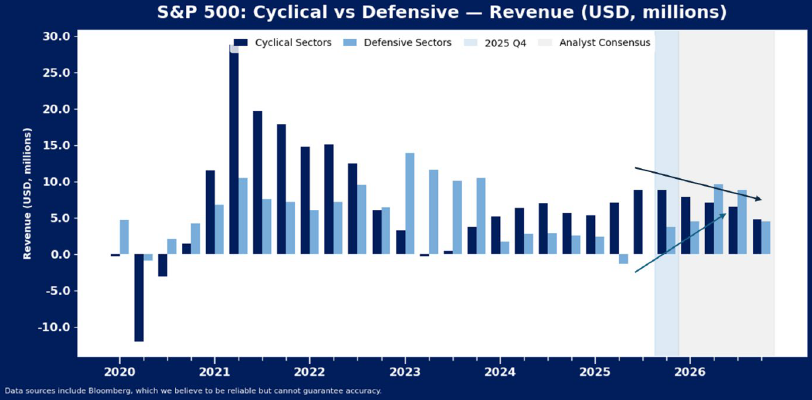

Large Cap Defensive Sectors May Start to Outpace Cyclicals

While revenue growth for the S&P 500 as a whole might stall out at a relatively heady pace of growth this year, there is an internal rotation in leadership that is set to emerge. After trailing cyclical sector growth since 2024, defensive sectors in large caps may start to show some revenue improvements in 2026. Analyst forecasts currently suggest that year-over-year cyclical sector revenue growth may have peaked in the fourth quarter, but defensive sector revenue growth is expected to continue to accelerate for at least the next few quarters, explaining some of the rotation that has been evident in U.S. large caps so far this year.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.