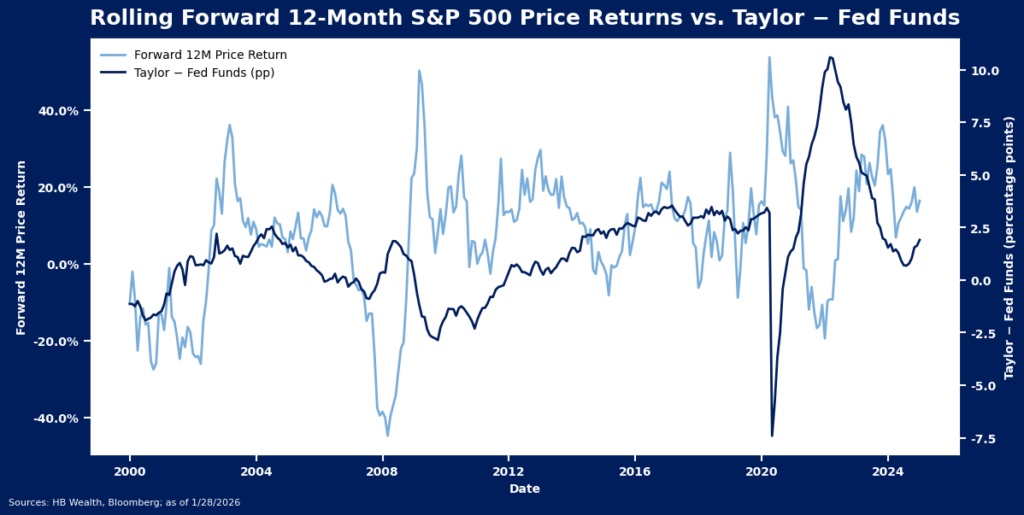

The FOMC paused rate cuts in January, with stabilizing labor markets and inflation pressures offering little reason to ease more at the current time. They didn’t need to ease more to stay easy anyway – after three consecutive declines in the benchmark rate in late 2025 the Taylor rule suggests policy is in accommodative territory. The spread between the Taylor rule and Fed funds is north of 2% currently, above its 25-year average of 1.5.

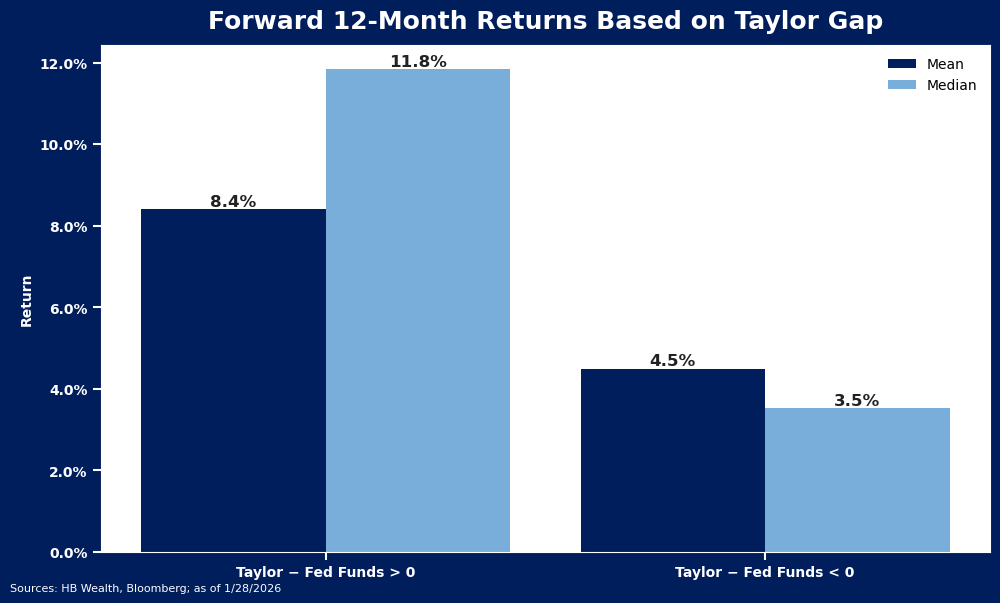

Stocks may not like the move much – we estimated earlier this year that equities were holding out hope for up to 4 cuts to emerge this year, and that seems increasingly unlikely. However, the current level of accommodation still sets a positive backdrop for equities. The market has averaged a 8.4% forward 12-month return when policy was accommodative (Fed funds rate below the rate implied by the Taylor rule), and a 4.5% forward 12-month return when policy was restrictive (Fed funds above).

The Fed did leave some hints in the post-meeting statement regarding what they may need to see to resume easing in future months. Policymakers said the “unemployment rate has shown some signs of stabilization”. This contrasts language in the last three statements that pointed to downside risks to employment as a concern and suggests jobs figures may have the biggest sway in future policy decisions.

With the Fed meeting now in the past, the market will quickly turn its attention back to earnings as a primary driver of prices in the near term. Mega cap tech stocks face lofty expectations for near 30% growth in 2026 and will need to justify those expectations to keep stocks powering higher.

Disclosure: HB Wealth is an SEC‑registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.