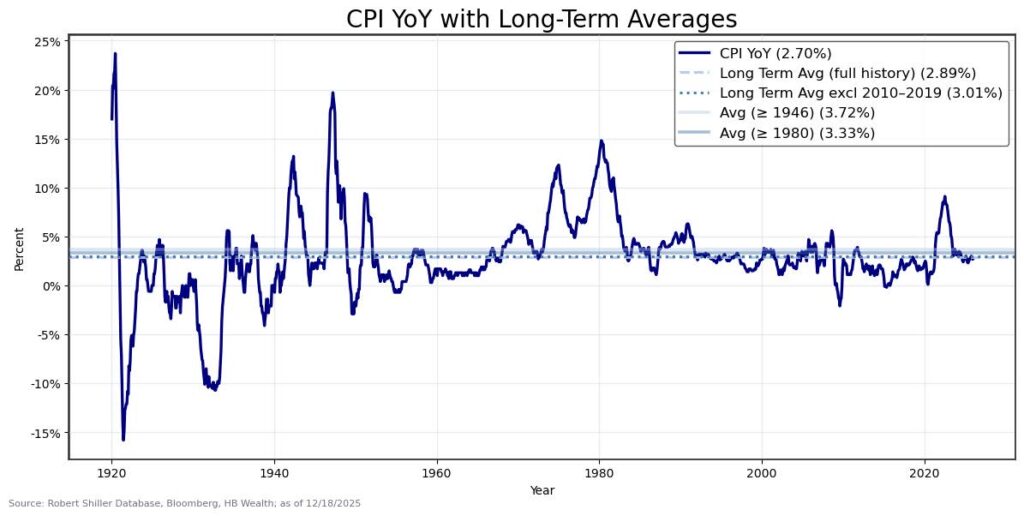

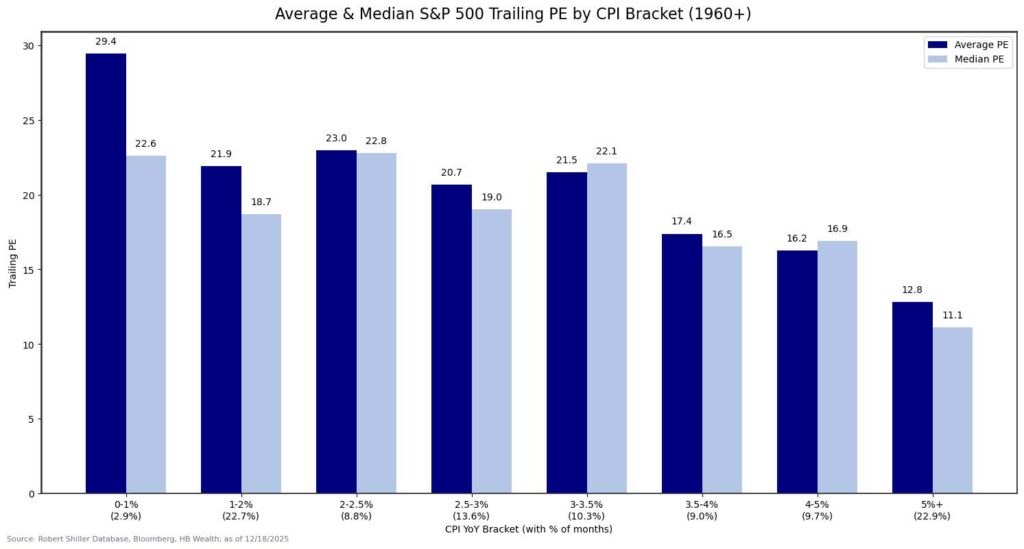

After rising for the bulk of the summer, consumer prices finally eased somewhat this fall, and the consumer price index (CPI) hit its slowest pace of growth since 2021 in November. It is too early to call an “all clear” on inflation risks, as autumn data may be somewhat distorted by the government shutdown and this year’s monetary, fiscal and trade policy shifts could still pressure prices higher in the year ahead. Lower inflation will likely need to persist to help support equity valuations. The current multiple at 27X is already well above the 19-20X that on average occurred with CPI in its current range. Yet, multiples were not historically negatively impacted until CPI rose above 3.5%.

Consumer price inflation (at 2.7% in November) is now back below its long-term average growth pace of 2.9%, and if it holds there, it could help justify Fed easing toward a terminal rate near 3%. Over the very long term (since 1920), year-over-year growth in the consumer price index (CPI) has averaged 2.9%. Excluding the deflationary scares of the Great Depression and the Great Financial Crisis, the average is 3.6%. And since 1982, the average has been 2.9%. So, no matter how we slice the data, 2.7% is slightly below long-term average inflation.

Stocks are already trading at multiples well north of what is justified by inflation. S&P 500 multiples averaged 20.7X in the current inflation range of 2.5-3% since 1960. The current multiple of 27X is above all experiences except the inflation range of 0-1%, when equity market multiples averaged 29.4X. The equal weighted S&P 500 index multiple, at 22X, is closer to the inflation regime norm implied by history but also is already higher than the level justified by inflation historically. However, historical patterns suggest that meaningful derating has typically occurred when inflation rises above roughly 3.5%. Stocks multiples historically ranged between 19X-23X when inflation was anywhere between 1-3.5%, but material drops in valuation were experienced with inflation above 3.5%.

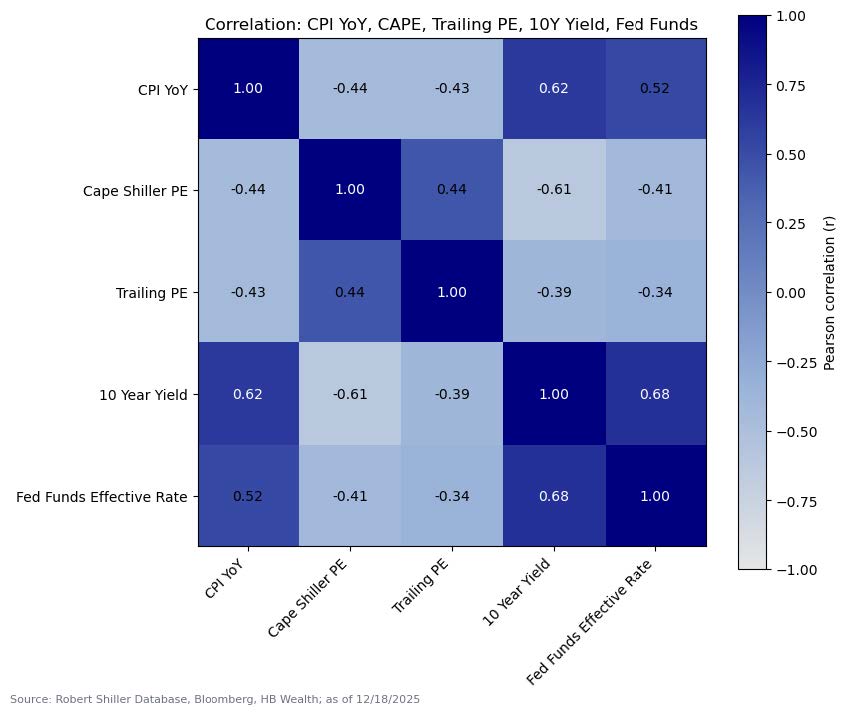

While the current level of inflation does not imply much by way of upside for stocks valuations, the direction of change as well as the level matters for equity markets, so we cannot simply rule out the potential for positive price impacts to emerge, particularly if inflation quiets enough to decrease interest rates. Consumer prices have relatively strong correlations with equity market valuations over time, and correlations between CPI and stocks’ PE, both on a cyclically adjusted and unadjusted basis, is negative. When inflation accelerates, it tends to suppress valuations, and vice versa. The correlation between CPI and interest rates is even stronger, so if lower price inflation keeps a rise in bond yields at bay and enables the Fed to decrease short-term interest rates, stocks could still benefit from some inflation reprieve.

HB Wealth is an SEC Registered Investment Adviser and the information provided is for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security, cryptocurrency, or other financial instrument. Digital assets, including cryptocurrencies, are highly volatile and may not be suitable for all investors. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. The views expressed are those of the author and do not necessarily reflect the opinions of HB Wealth. Comments for this post are not monitored. Please consult your financial advisor before making any investment decisions.