")

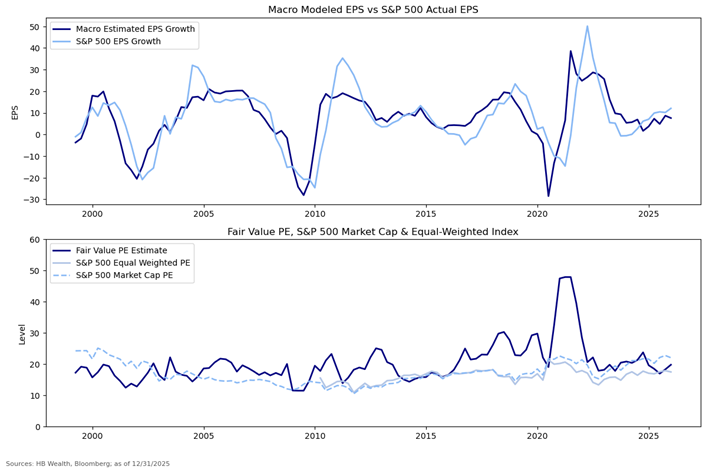

January events could set the tone for stocks in the year ahead, as elevated market multiples imply both the Q4 earnings season and FOMC Meeting are likely to be critical moments that set the stage for equity market direction. Given valuations for the market are well north of levels justified by current macro conditions, either earnings need to soar much more than the consensus expects, or the Fed needs to firmly state a path to easy policy to keep the bull market intact to start the year.

Even though stocks generally perform well when the Fed is easing, the current bond market forecast suggests it may still be difficult for the Fed to be able to satisfy stocks’ hopes. All else equal, the current market multiple north of 22X suggests stocks may already be priced for at least 100 basis points of additional cuts from the Fed. If the bond market is right to suggest about half of that is likely in 2026, this supports a market multiple for US stocks that is less than 20 times earnings, according to our model.

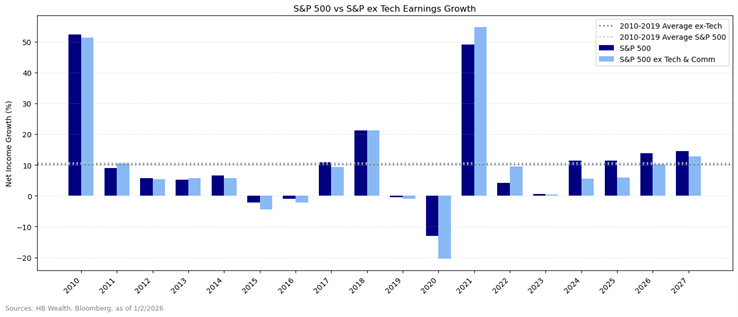

If the Fed cannot provide stocks as much monetary support as is expected, the onus will be on companies to stage an extraordinary earnings comeback to keep the rally intact. Over the last two years, macroeconomic conditions have supported just under 6% average growth in ex-tech earnings, with tech stocks kicking in growth of about 25%, resulting in average net income growth for the index of 11% in both 2024 and 2025. Assuming economic conditions improve in line with economic consensus, a moderate acceleration in ex-tech growth could emerge in 2026. Our model says 8% growth in S&P 500 earnings is a reasonable expectation for the year, and the bottom-up consensus says 10%. However, this will not be enough to justify current valuations with only modest Fed support. To justify current multiples with just 2 rate cuts, US large cap stocks may need to put up 30% earnings growth over the next year. Thus, if the Fed is unable to comply with lofty expectations for easing, a lot of optimistic corporate profits outlook commentary will be needed in the reporting season just ahead.

Disclosure: The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.