International shares outperformed US large cap stocks by the most since 2007, and developed markets topped US stocks by the most in more than three decades in 2025, helped by flight from the dollar and valuation expansion. Earnings will likely need to kick in support to keep the party going for non-domestic stocks in 2026.

The group’s performance was helped by a near 10% annual decline in the dollar, the most since 2017. Back then international stocks also outperformed the U.S., but by less. This time developed markets like Canada and Europe are benefitting most from the dollar debasement trade.

As interesting as the dollar story was, last year’s global equity performance hinged more on valuation expansion than currency. More than half the gain in markets like China, Europe, EM Latin America, and ASEAN.

That valuation bump suggests the policy boost and improving earnings growth prospects likely drove stocks returns. So, while continued geopolitical uncertainty may remain a tailwind for currency to elevate international equities, earnings may also need to recover smartly to keep the party going for non-domestic shares.

The Dollar May Help, But Earnings Will Also Need to Make the Case for International Stocks

International shares outperformed US large cap stocks by the widest margin in years in 2025. The group’s performance was helped by the dollar’s decline – uniquely, developed markets like Canada and Europe benefit most from the dollar debasement trade. However, last year’s performance hinged largely on valuations, suggesting a combination of policy support and improvement in expected earnings growth was also responsible for the gain. Geopolitical uncertainty may remain a tailwind for currency to continue to elevate international equities performance, but after 2025’s valuation expansion, earnings may also need to recover smartly to keep the party going for non-domestic shares.

Dollar is Altering Global Equity Investment Landscape

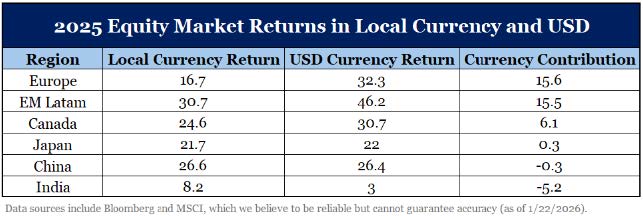

The dollar dropped 9.4% in 2025 – its biggest annual decline since the near 10% drop in 2017. While dollar weakening helped propel global shares to some degree, its contribution to return was particularly strong and unusual for developed markets. The table below shows 2025 returns across the major equity markets in local currency compared to returns in USD. All but India outperformed US stocks, in both local and dollar terms. Europe was notably the biggest beneficiary of the drop in the dollar last year; in local currency, the market outperformed the US by just a few percentage points, but in dollar terms, Europe nearly doubled the return of the US.

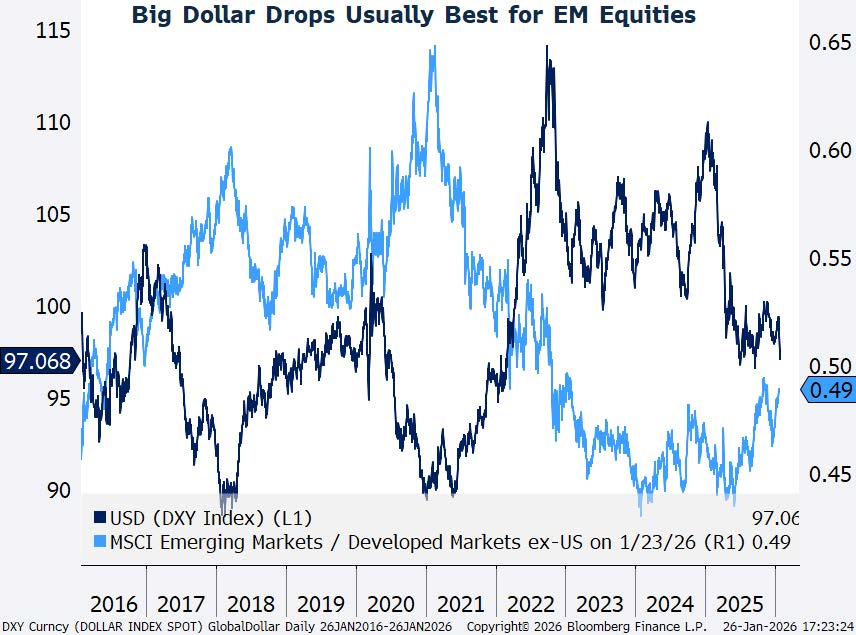

It is unusual for developed markets outside of the US to be the bigger equity market beneficiary of dollar weakness. Historically, dollar declines have benefited emerging markets the most among major segments in the global equity sphere. Indeed, back in 2017, when the dollar last dropped as much as it did in 2025, EM equities were the better performing markets, with China and India topping the charts.

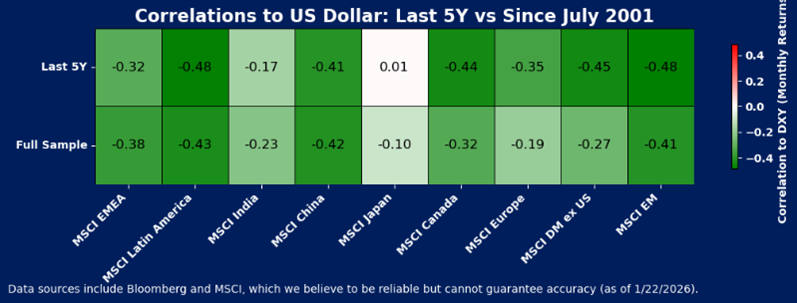

Correlations data likewise shows that in the long run, emerging market equities have traded more closely with the dollar than developed market equities. Latin America, China and EMEA have among the most negative long-term correlations with the dollar. However, correlations have shifted somewhat in the last five years. Developed markets’ performance has become more closely correlated with currency movements.

The fact that the dollar drop coincided with strong shifts in equities in developed markets in recent years, and especially in 2025, may say something about dollar debasement themes starting to work their way into the global equity markets. If so, a broader subset of international equities may remain beneficiaries of ongoing rotation away from dollar assets.

Valuation Expansion Drove Gains in 2025

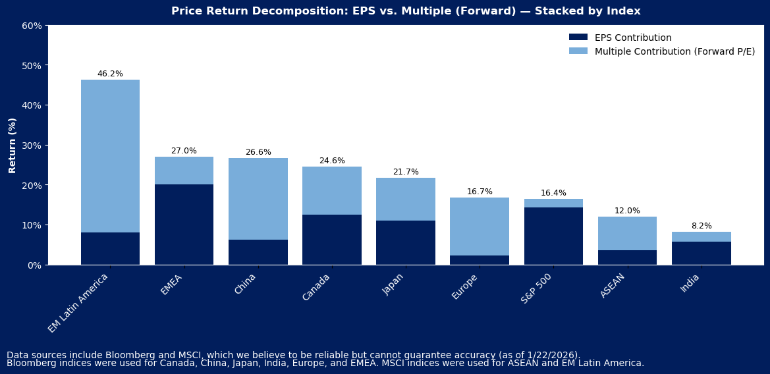

However, the dollar is not the only factor that matters for international equity performance. While the dollar helped elevate global stocks returns in 2025, valuation expansion was the primary driver of the reversal of fortunes for non-domestic equities. A breakdown of returns (in local currency) shows that most of the return in almost all global equity markets outside of the US came from valuation expansion in 2025. Among the major markets, earnings drove more than half of price returns for only the US, Canada, and Japan last year. Emerging markets in Latin America, China and ASEAN had the greatest share of price return come from valuation expansion, and almost all of European price growth was due to multiple expansion. Broadly, emerging markets derived 47% of their 2025 equity market price gain from expansion in market multiples, while developed markets (outside of the US) had 51% of price return driven by valuation expansion.

The global valuation expansion is likely partly due to the combination of central bank support (which also plays out in currency), and projected future earnings growth, some of which is driven by fiscal policy expansion. Notably, most central banks reduced interest rates in 2025, and many did so faster than the Fed. Fiscal spending plans also broadly accelerated, in large part due to geopolitical uncertainty driving elevated defense spending globally.

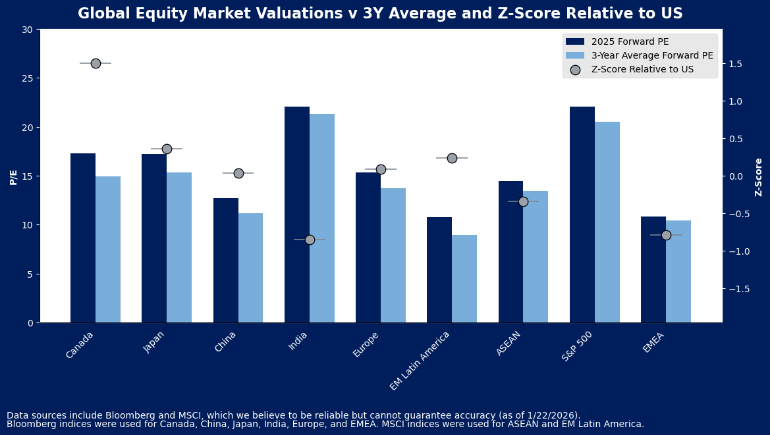

After the re-rating that occurred last year, most major world equity markets are now trading well above 3-year average valuations, suggesting less room for valuation expansion to drive price appreciation in global shares. However, the relative rating landscape is different. All major world equity markets are still discounted to the US. Canada and Latin America’s discounts to the US are slightly below average, but all other markets retain above average discounts to US stocks, some analysts believe rotation could continue, but outcomes remain uncertain.

Earnings Growth May Need to Help Drive Prices in 2026

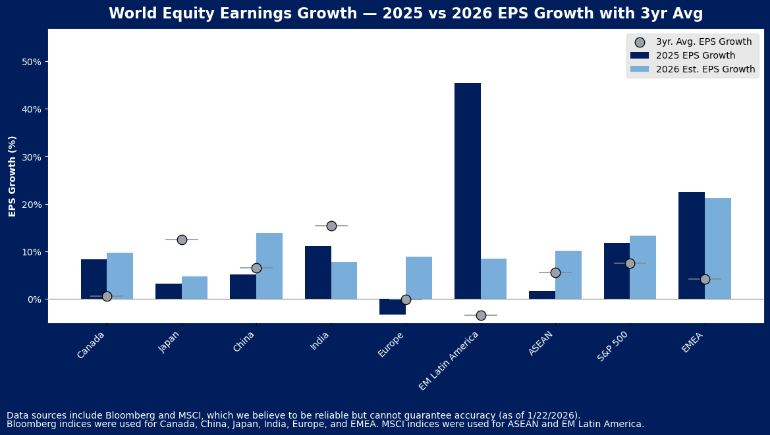

With less room for absolute re-rating to continue to drive share prices, current valuations imply the international equity markets may need an acceleration in earnings growth to also help drive returns in the year ahead. Whether through monetary and fiscal policy support or organic growth, valuations imply the market expects profits recovery, and analysts now anticipate a growth revival will emerge in many markets around the world in 2026 as well. Five of the 9 major market segments are expected to record faster earnings growth in 2026 than in the year just past. Likewise, 7 of the markets are expected to record stronger than 3-year average growth, with only Japan and India still lagging the norm. Yet, just 2 markets – China and EMEA – are expected to grow earnings faster than the US.

Conclusion

While the declining dollar was a support to non-domestic stocks in 2025, and currency could continue to enable better performance for non-domestic stocks, the path to progress for these markets is not likely entirely currency dependent. After a year in which valuations largely drove price returns, earnings growth improvements may need to also help make the case for rotation outside of the US. Valuations suggest higher than usual expectations for growth improvements have emerged, even if they remain somewhat underpriced by comparison to the US. Thus, non-domestic markets may need more than currency to keep markets afloat in 2026 and must offer solid earnings growth prospects for their stocks to continue to shine.

Disclosure: HB Wealth is an SEC-registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.

How to Talk to Your Children About Wealth

Overcoming Reluctance and Strengthening Family Wealth Communication Many families avoid discussing wealth in an effort…

Read More