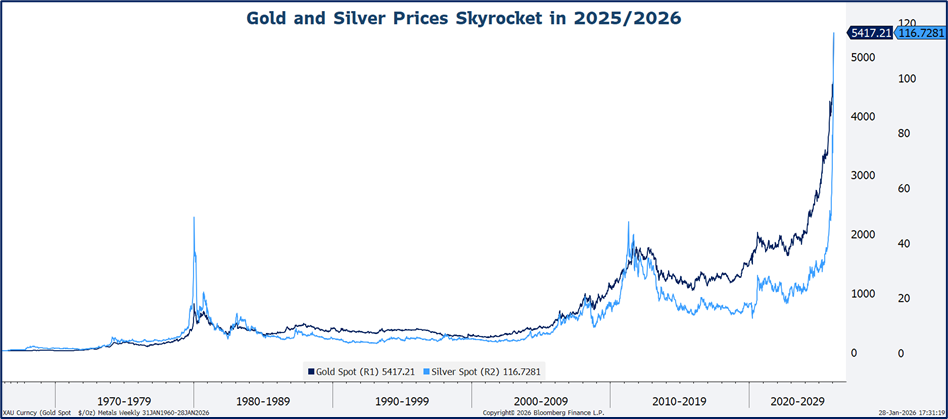

Metals prices are breaking records so far in 2026, hitting new all-time price highs and recording rates of price change last touched in 1979. Back then, prices rose until higher interest rates and a painful recession emerged. This time, gold might continue to run until geopolitical stability or an effort to stabilize the dollar surfaces. Silver’s surge may get under wraps only when energy and electronic production slows down.

Gold is traditionally a safe-haven asset and store of value, thus it gains support when the dollar weakens and when geopolitical uncertainty rises. Currently gold is serving both as a debasement hedge and in its more traditional role as competitor to U.S. Treasuries and money market funds, where yields have been contained with the Fed easing policy. Silver’s resurgence, in contrast, is more about industrial demand. The metal is an essential production component in solar energy, electronics and grid infrastructure.

Production cannot keep pace with growing demand in either market, thus, prices are accelerating. Metals mining is a slow, capital-intensive industry with growing constraints. This means that as prices surge, new supply cannot be brought online easily. Global gold mine output has increased only incrementally in recent years. Energy costs are rising, and new discoveries are rare. The silver market is even more constrained, with most global supply a by-product of base metals like copper, lead, and zinc.

The 52-week rate of change in both metals is in rare territory – gold has nearly doubled in the last year and silver jumped more than 3X, rates of change that have only occurred once in recent history – in 1979. Back then, geopolitical risks were also elevated and inflation concerns predominant. It took a Fed hike to break demand and slow the metals down. With supply structurally constrained, it will again likely take a break in demand to slow growth in prices. This could come from an increase in rates, geopolitical stability, an effort to stabilize the dollar, or in the case of silver, a slowdown in industrial production.

Disclosure: HB Wealth is an SEC‑registered investment adviser. The information reflects the author’s views, opinions, and analyses as the publication date. The information is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any investment product. This information contains forward-looking statements, predictions, and forecasts (“forward-looking statements”) concerning the belief and opinions in respect to the future. Forward-looking statements involve risks and uncertainties, and undue reliance should not be placed on them. There can be no assurance that forward-looking statements will prove to be accurate, and actual results and future events could differ materially from those anticipated in such statements. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. Certain information herein is based on third-party sources believed to be reliable, but which have not been independently verified. Past performance is not a guarantee or indicator of future results; inherent in any investment is the risk of loss.