As a wealthy family, the question of whether to have a “family office” will inevitably arise, whether from wealthy friends, advisors, articles about other wealthy families, networking groups, or all the above. You will also likely hear differing opinions about whether to establish a single-family office, utilize a multi-family office, or possibly explore ‘hybrid’ solutions somewhere in between. To help families best understand their options, over the coming weeks, we will be sharing our experiences in a series of short, practical segments outlining key considerations. Let’s start with the basics: What is a family office?

The Definition

Defining a family office can be approached in various ways, often resulting in an extensive list of services provided. We define a family office as a coordinated team of staff and advisors dedicated to managing the financial affairs of a complex or multi-generational wealthy family. As we will discuss in a future blog, this can be a dedicated staff working only for the family (a Single-Family Office or SFO), or it can be a group of professionals who work for more than one family (a Multi-Family Office or MFO).

Family Offices Are Not New

The idea of having a family office is not a recent concept. Some form of a “family office” likely existed back as early as the days of the Renaissance, where successful families, such as the Medici, surrounded themselves with advisors to help manage their family affairs across a wide range of business and philanthropic pursuits. The more recent American version of the family office concept emerged with the wealthy families of the late 1800s and 1900s when families like the Carnegies, Rockefellers, and Vanderbilts amassed great wealth that required a dedicated staff to help them manage their affairs across businesses, charitable giving, and multiple generations.

Family Offices are Growing and Evolving

The creation of family offices and their scope has increased and widened over the past 50 years, as a wider set of families created wealth after World War II. Historically, the primary focus of a family office has always been financial – managing family investments, handling taxes, planning for future wealth transfer, coordinating philanthropy, and ensuring these matters are handled across generations. Over time the mandate of a family office has often broadened to incorporate more multi-generational efforts such as financial education, family governance, concierge lifestyle services, health and wellness, and other aspects of family life.

What Services Does a Family Office Provide?

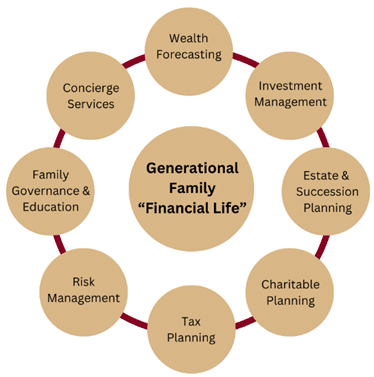

As described above, the family office is focused primarily on managing and coordinating the “Financial Life” of the family across generations. This generally includes wealth forecasting, investment management, estate planning, charitable and tax planning, risk management, family education/governance, and concierge services.

Wealth forecasting involves long-term cash flow modeling applying various assumptions to project the implications of family planning decisions, investment allocations, and risk scenarios. The wealth forecast discussion serves as the foundation for numerous planning topics and offers families a continuous resource (i.e., a planning benchmark) to evaluate the near- and long-term impact of their decisions.

Investment management is often assumed to be the primary role of a family office, but in reality, it may or may not be the top priority each day. This includes setting an appropriate asset allocation for each family entity or family member, choosing the investment advisors or asset managers to implement the strategy, and providing consolidated reporting across all investment assets to the family. The last part (reporting) is often a major task for some family offices, given the complex web of investment relationships and ownership structures families have built over time. Investment management also includes managing the inflows and outflows administratively for each investment, including handling capital calls, paperwork and other cash flow needs of the family.

Estate and succession planning involves working with the family to define their planning goals and help determine which tools and strategies will best help them achieve those goals. This often involves coordination across multiple tax, legal, and business specialists, and may involve utilizing both outside and in-house counsel for legal drafting and implementation. With constantly changing estate and business laws, families need to regularly revisit and update their plans, even if they believe their previous planning was thorough.

Charitable planning incorporates a wide range of options for philanthropic family efforts. This may include determining the right structure for giving directly or creating a pool of future charitable capital, deciding how to best optimize the tax benefits of potential gifts, or simply deciding how to prioritize what types of gifts to make and how to negotiate those gifts if they are significant.

Tax planning interacts with all facets of the family office work, as almost every decision made has potential tax implications now or in the future. Tax planning may include in-house preparation of tax returns or may involve the use of an outside CPA. Both approaches involve managing the yearly schedule and processes of tax compliance and strategically planning to reduce taxes over time.

Risk management addresses personal and property risks to protect the family based on their specific situation and assets. This can be as simple as ensuring appropriate and efficient property and casualty coverages across family holdings, or as complex as designing and maintaining sophisticated multi-family business buy-sell or wealth transfer life insurance agreements. Risk management has recently evolved to also include engaging specialty cybersecurity or even personal security firms to help address unique risks faced by the family.

Family governance and family education are broad and highly personal topics that will mean different things for different families. In some instances, this may address family business succession matters and managing a family business over multiple generations. In other cases, it may be focused on when to start sharing financial information with the next generation and how to ensure that they are informed financial stewards of that future wealth.

Concierge services can be as high level as recommending a good bookkeeper or travel advisor, or as granular as actually paying the family bills and booking their vacations! Concierge services are unique to each family’s needs, and some families seek to outsource more of these services to their family office than others.

What About Actual Tax and Legal Work?

As noted above, some family offices manage tax compliance (filing returns), entity accounting, and legal document preparation (estate, entity, etc.) via full-time employees who are attorneys and CPAs. This is an area typically included within the scope of the largest single-family offices. However, many family offices, even those structured as single-family offices, often outsource some or all of this function rather than managing it in-house.

What About Managing Houses and People and Paying the Bills?

Some people believe that if you are not managing the houses (or house staff), airplanes (or pilots), paying the bills, or managing other day-to-day events, then you are not truly operating a family office. This is truly a gray area and unique to each family. While some family offices transition from a CFO (or financially focused) role into a COO (or operations-focused) role, others do not. As the cliché goes, if you have seen one family office then you have seen….one family office.

The Bottom Line—A Family Office Ultimately Has to Fit Your Needs

Back to that cliché about every family office being unique – it really is true that the definition of a family office is what you want it to be. There is no formal certification to define what cluster of services qualifies as a “real family office.” The determination of what operational, professional, and personal services should be provided by your family office is ultimately up to you.

To learn more about a family office, please visit us at https://hbwealth.com/resources/understanding-family-offices/, send an email to info@hbwealth.com, or call 404.264.1400.

Important Disclosures

This article may not be copied, reproduced, or distributed without Homrich Berg’s prior written consent.

All information is as of the date above unless otherwise disclosed. The information is provided for informational purposes only and should not be considered a recommendation to purchase or sell any financial instrument, product, or service sponsored by Homrich Berg or its affiliates or agents. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. This material may not be suitable for all investors. Neither Homrich Berg nor any affiliates make any representation or warranty as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources believed to be reliable but are not guaranteed. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

©2025 Homrich Berg.