Ever since the passage of the “Tax Cuts and Jobs Act” (TCJA) in 2017, taxpayers, estate planners, accountants, and financial advisors have been working under a cloud of uncertainty. Many provisions had expiration dates, and the estate tax exemption was poised to drop sharply in 2026.

Now, with the passage of the “One Big Beautiful Bill Act” (OBBBA), we finally have clarity…for now. Among OBBBA’s most headline-grabbing provisions: a “permanent” increase in the federal estate, gift, and generation-skipping transfer (GST) tax exemptions to $15 million per person, to be indexed for inflation after 2026. This removes the much-discussed 2026 exemption “cliff” from the immediate horizon.

Does this all mean you can breathe a sigh of relief and put off estate planning until later?

Absolutely not.

Whether your net worth is $1 million or $1 billion, now is a critical time to review, modernize, and, where appropriate, streamline your estate plan.

A Brief Refresher on Estate Tax Basics

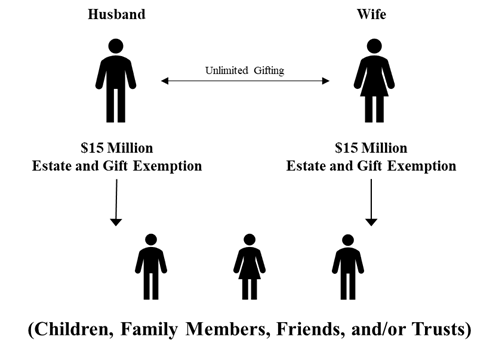

Your “taxable estate” includes everything you own, including but not limited to: cash, investments, real estate, business interests, retirement accounts, life insurance death benefits, and personal property. Married couples may pass as much as they would like to each other, completely gift and estate tax-free, but if they want to transfer assets to anyone other than a spouse, there’s a limit (the “exemption”) of how much may be transferred before gift or estate tax is imposed. Under OBBBA, each U.S. taxpayer may transfer up to $15 million (to be inflation-adjusted after 2026) during life, at death, or a combination of both, free of federal estate and gift tax. Married couples can effectively combine exemptions to transfer a total of $30 million to family and friends. Anything above the exemption amount passing to someone other than a spouse or charity is taxed at 40% (or even higher, if transfers are to grandchildren or younger generations).

Planning for Non-Taxable Estates

Many people assume that if their estate falls well below the $15 million mark, they can skip an estate update or review. In reality, OBBBA may have rendered your current planning outdated in ways that may cost your family avoidable taxes.

A significant number of married couples with older wills and trusts have a structure that automatically splits assets at the first spouse’s death:

- A Credit Shelter Trust (sometimes called a bypass trust) is funded first with an amount equal to the estate tax exemption at the time of the first spouse’s death. If a person’s estate is less than the estate tax exemption ($15 million), then many plans will direct the entire estate into the credit shelter trust, and a marital trust (described below) will not be created.

- A Marital Trust holds all assets in excess of the estate tax exemption (not in the credit shelter trust).

This structure made perfect sense when the exemption was much lower, when a central planning goal was focused on deferring estate tax, and when “portability” (the ability of a surviving spouse to use the deceased spouse’s unused exemption) did not exist. Today, with the overwhelming majority of Americans not having taxable estates, this traditional Credit Shelter Trust/Marital Trust structure may lock in unnecessary estate tax planning at the expense of income tax planning. How? To understand this, you need to first understand what it means to have a “step up” in basis.

| Step Up in Basis Let’s say you bought a house 15 years ago for $300,000 and, today, that house is worth $1,500,000. You have decided to sell the house for today’s value for a gross profit of $1,200,000. Before you uncork the champagne, keep in mind that you would owe the government capital gains taxes on the difference between your $300,000 purchase price (your “basis” in the property) and the sales price[1]. If, instead, you don’t sell the house and still own it when you die, your basis will be instantly transformed (or “stepped up”) to the fair market value of the house on your date of death. So, if your family sells the house after you die, they will not pay any capital gains tax on such a sale. $1,500,000 Sales Price – $1,500,000 [stepped up basis] = $0 Capital Gains Tax |

Returning now to the Credit Shelter/Marital Trust structure baked into so many plans: If you pass with a $6 million estate, all of which flows under the terms of your will into a credit shelter trust, that trust receives your stepped-up basis in your assets. Let’s say that, after you pass, your wife lives fifteen years more, and the value of the assets in the credit shelter trust grows to $13 million. When your spouse passes, the credit shelter will have done its job of allowing the assets within it to avoid estate tax, but those assets will not receive a step up in basis when your spouse dies because they were not owned by him or held in a structure for his sole benefit; instead, they were owned by a trust that maintains the basis of those assets upon receipt. In other words, after both spouses pass, your family will have avoided estate tax, but they will have to pay capital gains tax upon the sale of trust assets.

A more modern and common approach to estate planning that may rectify this capital gains issue is to include flexible provisions in your wills and trusts that allow the surviving spouse or executor to select the best tax strategy at the time of the first spouse’s death, all as prescribed by a plan you design with your attorney. This adaptability ensures your plan works under today’s laws and remains eligible for a step-up in basis at each spouse’s death (thereby avoiding capital gains tax), but it also provides the ability to pivot if the rules change again and estate tax deferral becomes the order of the day.

Updating your will and trust may not be the end of your estate review. As recently as 2017, the estate exemption was just over $5 million. As a result, many more estates were susceptible to the estate tax, and estate attorneys coached thousands of clients to create irrevocable trusts and establish structures to help minimize or eliminate such tax. If your attorney prepared any type of irrevocable trust for you, or if an irrevocable trust was established for you or a family member as a result of a gift or a death in the family, you may want to consult with your attorney about whether any such trust should be unwound or modified (as permitted), or whether there are actions you may take to reverse any unnecessary tax ramifications associated with a once appropriate, but now potentially burdensome, plan.

Don’t forget, during this review, to ensure your beneficiary designations and asset titling are all appropriate and work in coordination with your estate plan – old or new.

Planning for Taxable Estates

With the exemption now set at $15 million per person, many affluent families feel less urgency to plan, but reality suggests that the pressure is on:

- “Permanent” may not be permanent. A gambler will likely consider it a safe bet to say that the new exemption will remain in place for the rest of President Trump’s term in office, but all bets are off after that. Congress may certainly reduce the exemption in the future.

- Growth can push you over the line. An estate valued under $15 million today may easily exceed the exemption sooner than you think due to investment returns, business growth, or appreciation.

- Tax savings require time. Many advanced strategies to maximize the transfer of tax-free wealth to your family are most effective when implemented years in advance.

If your estate is at, above, or projected to be above the exemption, consider using the current window to “lock in” today’s higher exemption through lifetime gifts. Strategies may include:

- Annual Exclusion Gifts – In 2025, you may give up to $19,000 per recipient – likely to be $20,000 in 2026 – per year without using any of your $15 million exemption. If you have a taxable estate, $19,000 may not feel like a lot to remove from your estate, but when you remove $19,000 per spouse for each child, grandchild, and/or trusts created for their benefit, it all adds up.

- Direct Payments for Education or Medical Expenses – Any amounts paid directly to a medical care provider or educational organization for any individual may be unlimited in value and do not consume your gift or estate tax exemptions.

- Larger Gifts to Individuals or Trusts – Large taxable gifts to irrevocable trusts may provide tax benefits, asset protection, and appropriate control over distributions.

Your wealth advisor can help model asset growth, liquidity needs, and gifting capacity, and coordinate with your estate planning attorney to structure gifts for maximum impact, both tax-wise and to accomplish your family’s long-term personal goals.

And remember, estate tax reduction isn’t the only priority. Preserving family wealth, protecting assets from creditors, avoiding probate, ensuring privacy, and providing for loved ones and charities remain vital objectives regardless of exemption levels.

The Cost of Doing Nothing

Now that you have read an article full of compelling reasons to review your estate plans immediately, you still may feel tempted to delay. Maybe you will wait until a day when you happen to feel like spending money to talk to a lawyer about death and taxes; but, before you run to Target, plan your next vacation, or organize your sock drawer, please remember that failing to update your estate plan (or passing away without one) may result in missed tax-saving opportunities, assets passing in unintended ways, family disputes, and court involvement.

OBBBA gives us a moment of clarity and opportunity, but tax laws are always subject to change. Now is the time to ensure your estate plan reflects today’s rules, avoids outdated structures, and stays flexible for the future. Whether your goal is minimizing taxes, protecting family assets, or advancing philanthropic causes, an up-to-date estate plan is one of the most powerful tools at your disposal. The best planning happens when tax laws are favorable, not in the scramble after they change.

[1] This calculation is simplified for illustrative purposes and does not consider changes in basis during the ownership of the house, the Section 121 exclusion, or other complicating factors.

To learn more or get help with your finances, please visit us at hbwealth.com, send an email to info@hbwealth.com, or call 404.264.1400.

Important Disclosures

This article may not be copied, reproduced, or distributed without HB Wealth’s prior written consent.

All information is as of the date above unless otherwise disclosed. The information is provided for informational purposes only and should not be considered a recommendation to purchase or sell any financial instrument, product, or service sponsored by HB Wealth or its affiliates or agents. The information does not represent legal, tax, accounting, or investment advice; recipients should consult their respective advisors regarding such matters. This material may not be suitable for all investors. Neither HB Wealth nor any affiliates make any representation or warranty as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources believed to be reliable but are not guaranteed. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

Key Economic and Investment Themes to Watch in 2026

As we look to 2026, this video shares our perspective on several key economic and…

Read More