Homrich Berg Unveils HB Wealth as New Name, Aligning Under Unified Brand

$25B RIA’s rebranding reflects national scale and client-centered focus ATLANTA, GA — August 19, 2025…

$25B RIA’s rebranding reflects national scale and client-centered focus ATLANTA, GA — August 19, 2025…

The Federal Reserve once again kept its key rate unchanged at its June 12th meeting….

Spring is my favorite time of the year. The gloom and cold of winter rains…

A strong job market continues to create challenges for the Fed to reach its 2%…

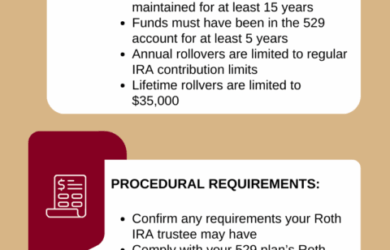

Download this infographic. To learn more about these requirements, please read this blog. If you…

One of the most talked about provisions of the SECURE 2.0 Act is the ability…

As we skip into springtime, we turn our attention to cleaning up our yards and…

Embarking on a solo journey after a significant life change such as divorce or becoming…

Since the Fed first signaled in early November that the rate hike cycle was likely…

Principals Ross Bramwell and Ford Donohue discuss inflation, the jobs market, the “Magnificent 7” stocks,…

Although it may seem like you’re alone, divorce affects one in five marriages. The “honeymoon…

Evaluating Business Structures: The Pros And Cons

Family businesses often start small with simple business and tax structures. However, as businesses expand,…

Read More